Video Clips

Quoted moments from Alaska public meetings, hearings, and press conferences.

0:12

Bert Stedman

“I think after January 1st, 60, 100% goes to the general fund, not community assistance. Is that right?”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

1:12

Adam Prestidge

“our practical expectation is that we will complete the project ahead of these timelines, and so the deadline or the timeline that you said The end of the year for FID maintains— continues to be our target. And we would— if we were to follow a target construction schedule, even with some delays, we would complete the project before December 31st, well before December 31st, 2032.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:26

Adam Prestidge

“That penalty is— would be losing the tax— the tax treatment of the project. The result of that would be at the front end, investors would look at this as additional risk, And they would have to price in that risk into how they invest in the project. And so the ultimate outcome of this would be making the project more expensive and require more investment capital.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:55

Adam Prestidge

“The 2032 completion of construction is more about managing theoretical risk that lenders and investors will look at when they make an investment decision on the project. And so regardless of how we all want to move fast, Regardless of the timing around the energy availability out of the Cook Inlet, lenders and investors will just see this numerically and assign it a hypothetical risk that will make the project more expensive. And so we don't see it adding any additional incentive that isn't there already. It just adds risk to the project that will be priced into the financing.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:25

Dan Stickel

“fixing the percentages does increase some of the certainty and makes it easier to calculate and plan. Removes one item of potential contention going forward.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:19

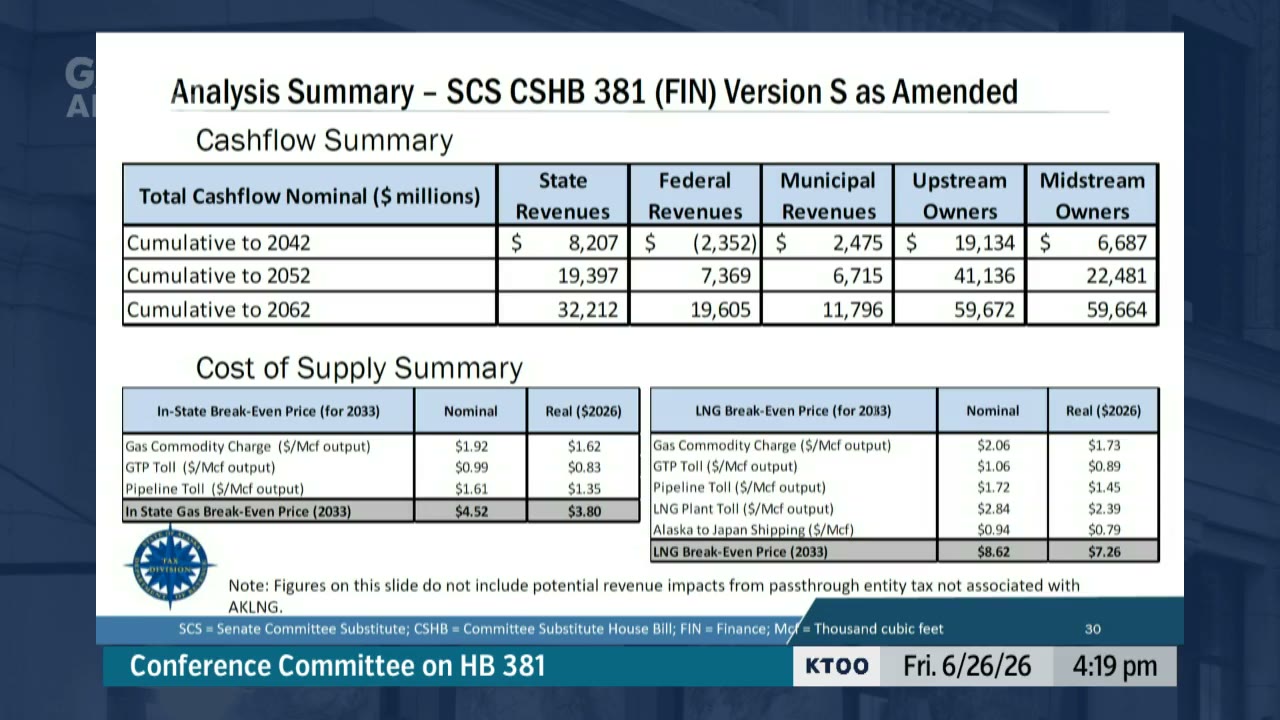

Dan Stickel

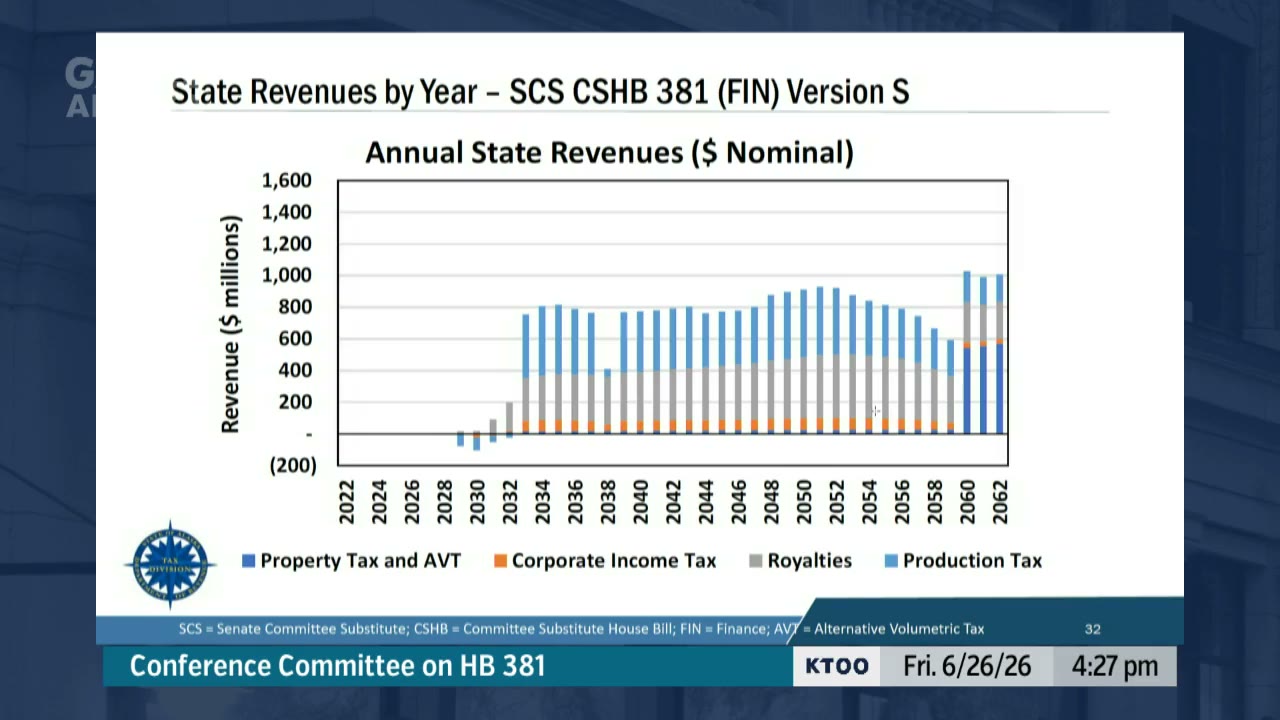

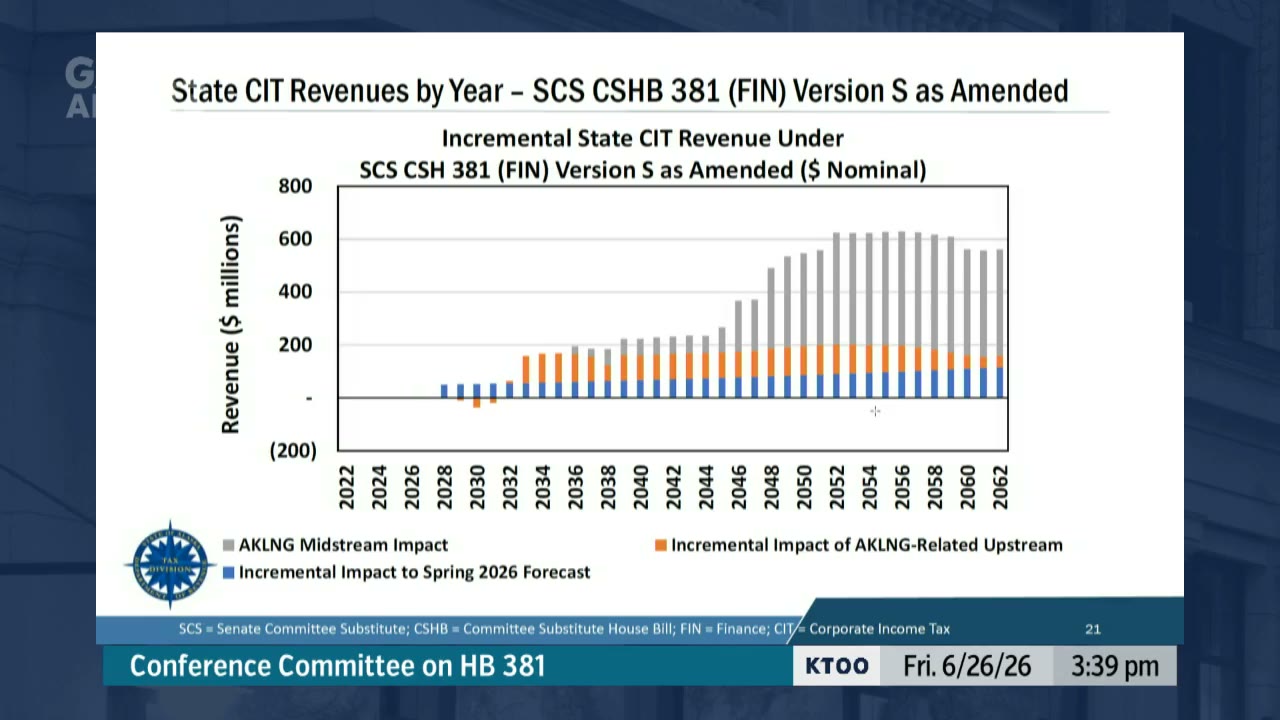

“total state benefits under our baseline model assumptions, which which we talked about yesterday, through 2042 would be $7.5 billion to the state.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:17

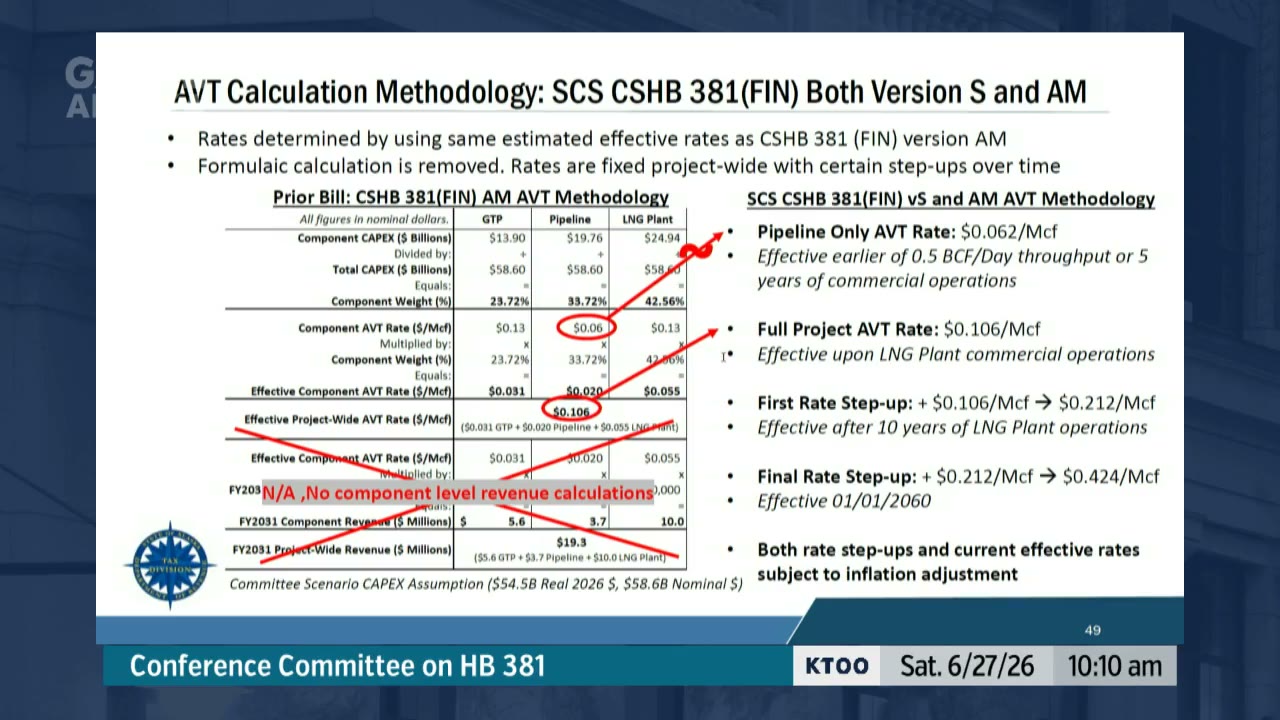

Dan Stickel

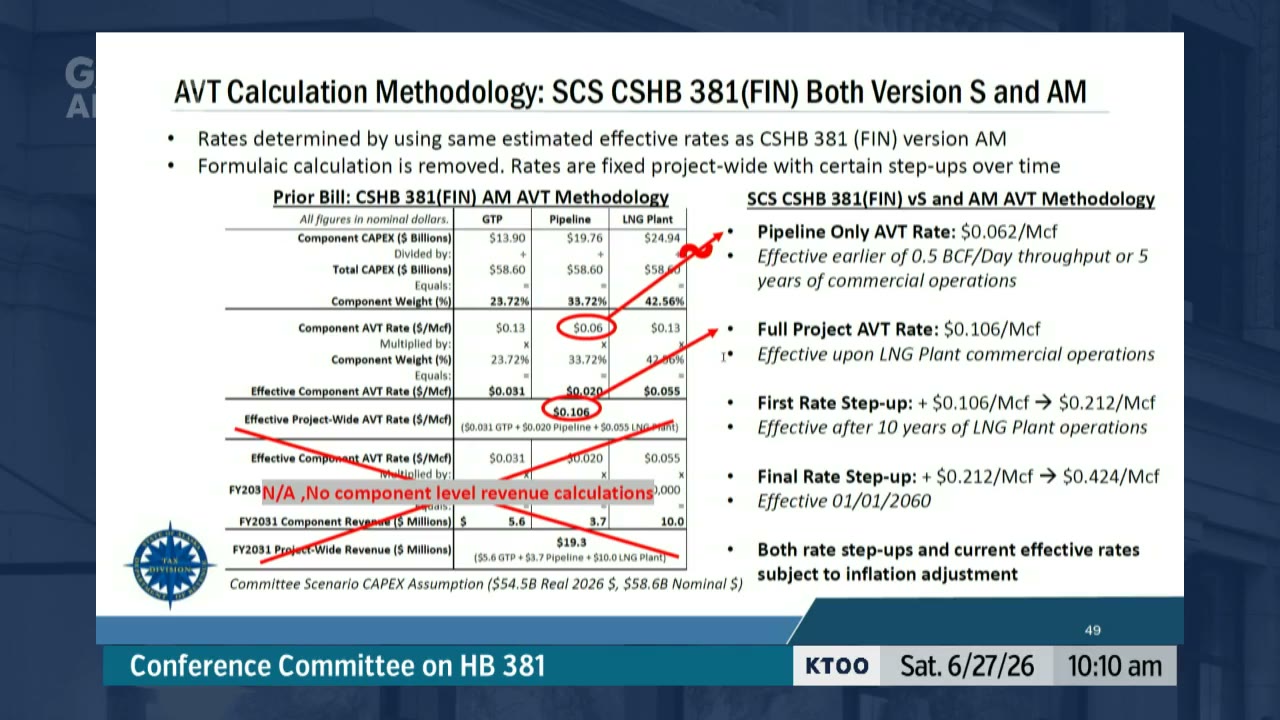

“It does start with the same effective tax rates as the House version and simply fixes those rates and allocations in, in statute. The Senate version then added in the two doublings of the tax rate that was a major change from the House version.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

1:01

Dan Stickel

“they moved away from this weighted average approach and instead just put in the flat rates for each component of the project. So they took that about 6 cents per MCF rate on the pipeline component and made that a 6.2 cents per 1,000 cubic feet tax rate for phase 1 of the project. And then they took that 10.6 cents per thousand cubic feet weighted average with the capital expenditures weighting and just made that the tax rate once LNG exports began.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:21

Dan Stickel

“the Senate version of the bill removes some of the complexity in the calculation that was in the prior version of the bill.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:13

Dan Stickel

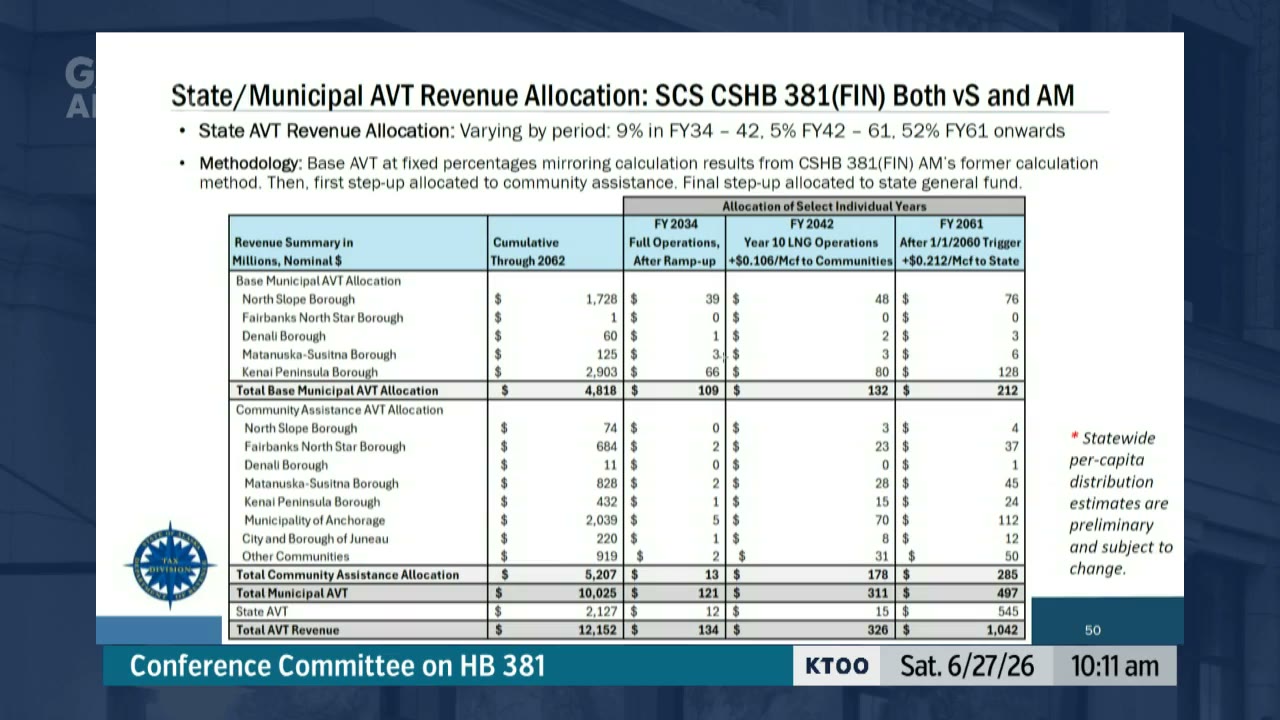

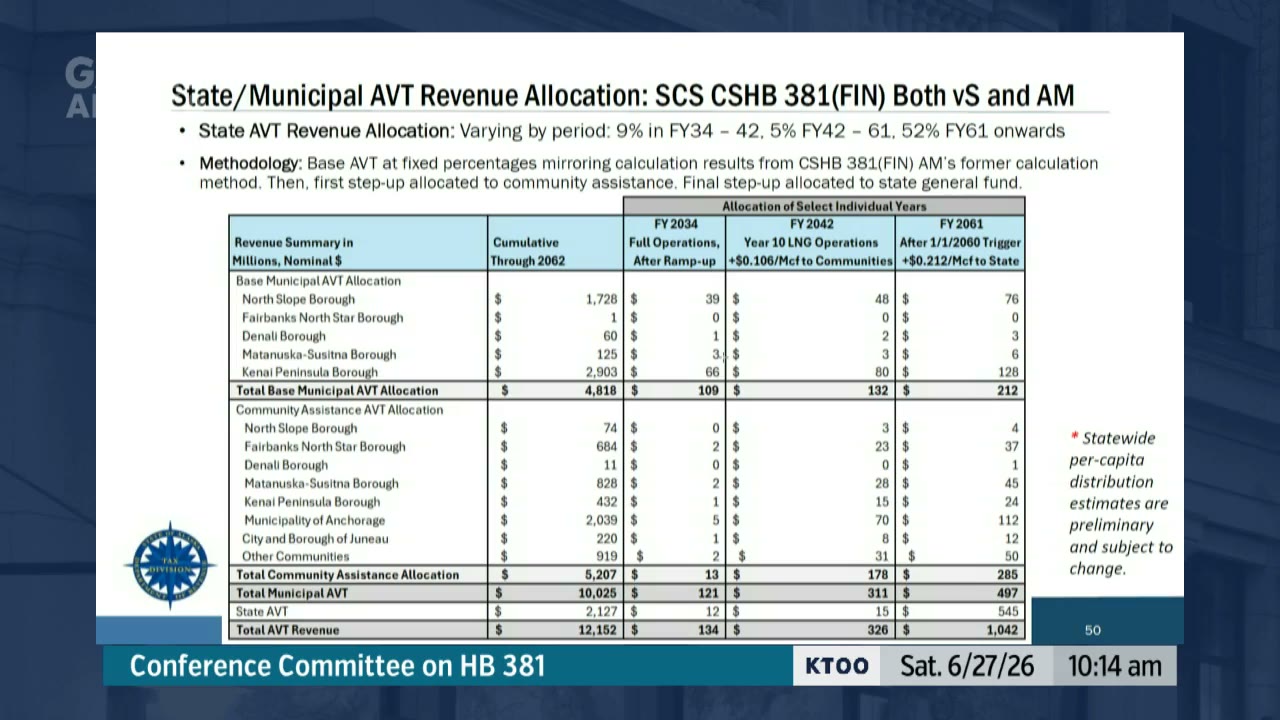

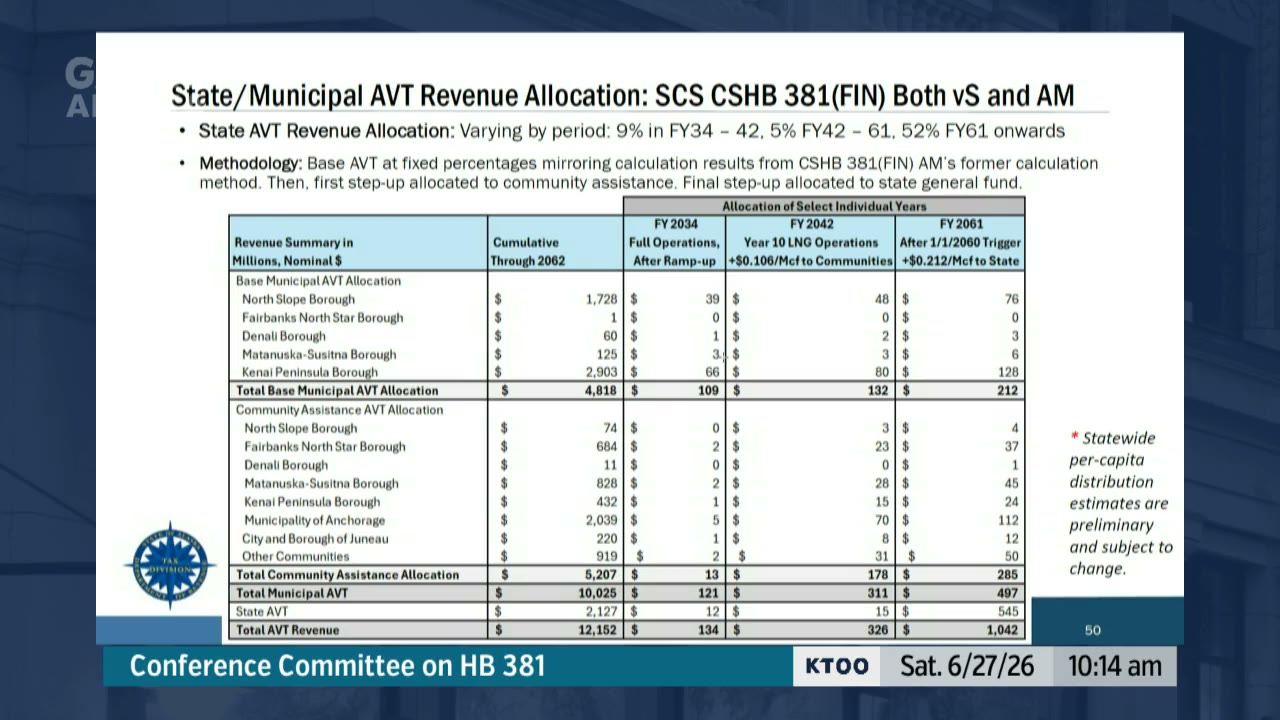

“for the first doubling of the tax rate, 100% of that doubling would go to community assistance, and then for the second doubling of the tax rate, 100% of that that next doubling would go to the state unrestricted general fund.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:21

Dan Stickel

“The first effective 10 years, after 10 years of LNG export operations, where the tax rate doubles. And then the second effective in 2060, where the tax rate doubles. Again.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

1:08

Dan Stickel

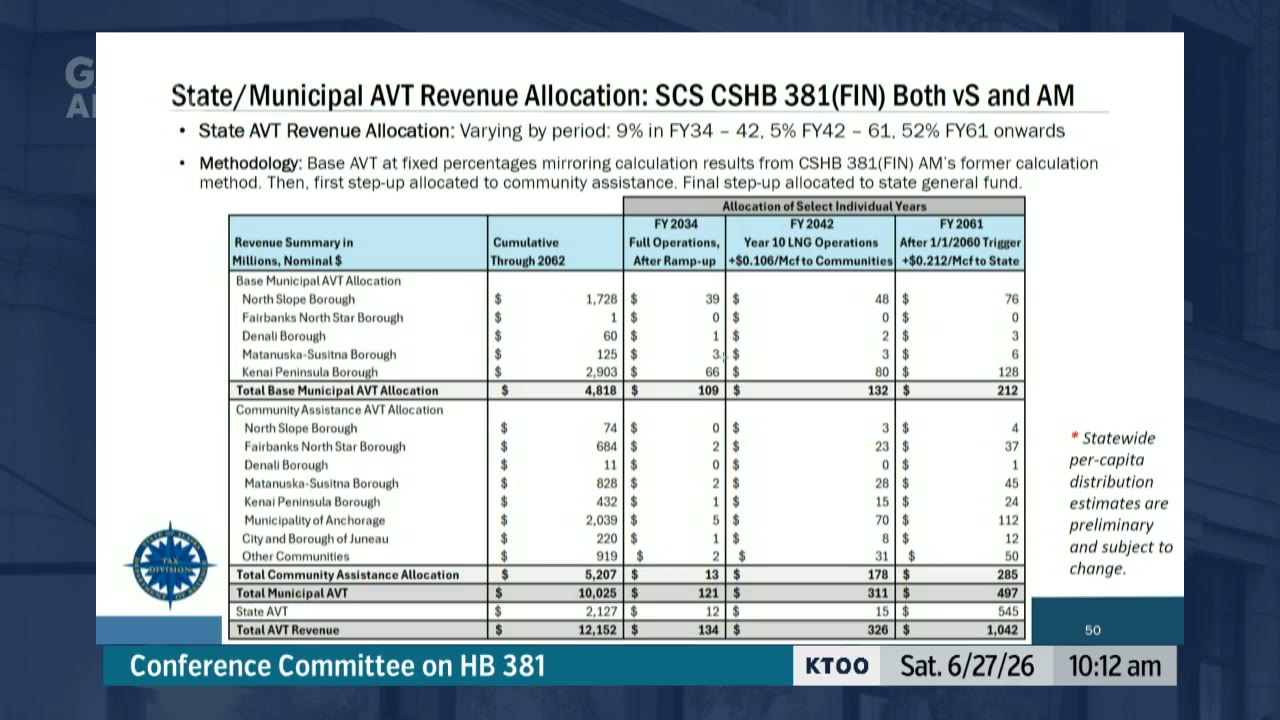

“in those early years, the vast majority of the revenue is allocated to the communities that the project is directly in. So $109 million of the AVT in 2034 would go to those 5 municipalities, with an additional $13 million spread statewide to community revenue sharing and $12 million to the state. And then the second column shows after the first step up in the alternative volumetric tax, and that additional step up goes entirely to community revenue sharing.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:38

Dan Stickel

“the state starts out receiving about 9% of the AVT revenue. That will drop to 5% with the first doubling of the tax rate.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:05

Dan Stickel

“But then increase to 52% of the total AVT with the second doubling of the tax rate.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:24

Dan Stickel

“for a pipeline-only portion of the project, you'd have a 6-cent per MCF tax rate, and then once the full project was in operations, we would estimate that the tax rate on a weighted average basis would be about 10.6 cents per 1,000 cubic feet.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:22

Mike Cronk

“if we do nothing, these numbers go away, we have nothing here. There's zero revenue brought to this state. There's zero revenue brought to many communities.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

1:14

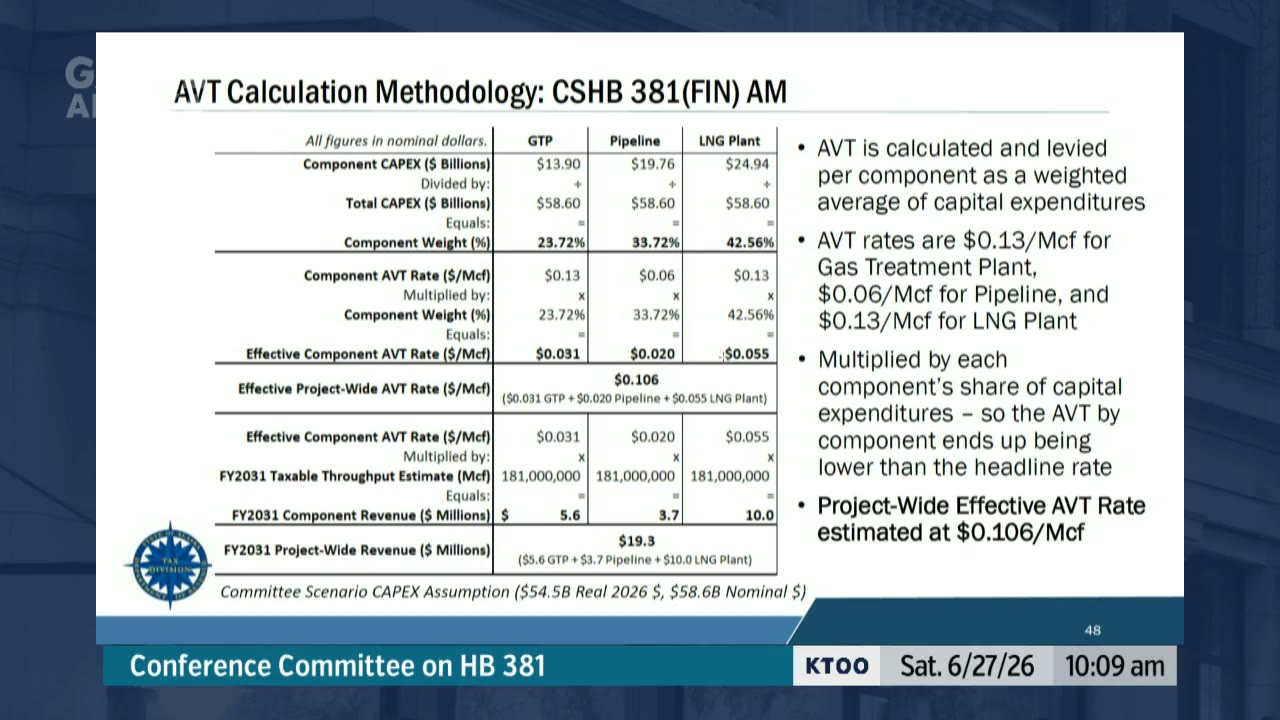

Dan Stickel

“under the House version of the bill, the alternative volumetric tax was calculated and levied on a per-component basis as a— using a weighted average of capital expenditures. And so once the full project was complete, we would look at the, the total capital expenditures that were spent on each component of the project, being the treatment plant, the pipeline, and the LNG export facility.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:30

Adam Prestidge

“we as the project developer at 8 Star have no objection to the 2028 FID deadline. We're only raising concerns around the 2032 completion of construction deadline.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:32

Dan Stickel

“the capital expenditure weighting and the project component weighting, that applied both for calculating the initial tax rates, but then also applied for calculating the sharing out to municipalities. And that sharing out to municipalities has also been fixed in statute. In the Senate version of the bill. So removing some of that complexity. The other addition that the Senate made is the two step-ups.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:28

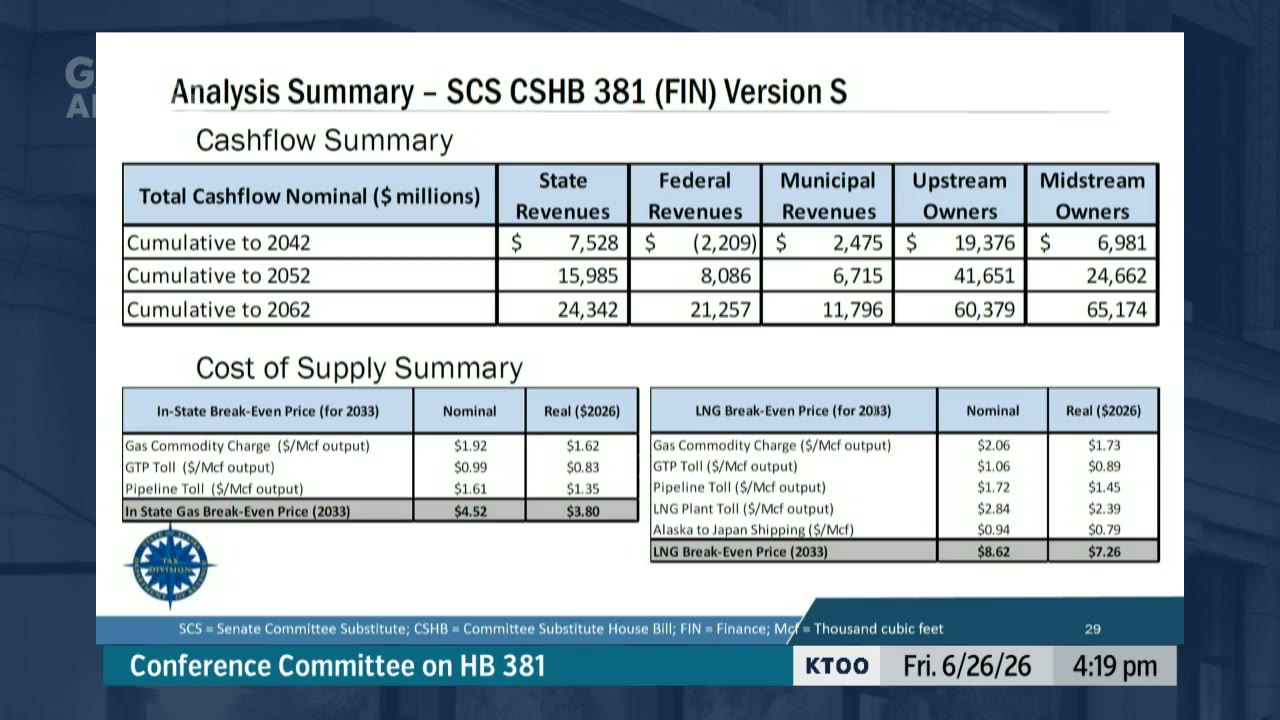

Dan Stickel

“through 2062, which is the to the extent of our modeling, $32.2 billion to the state. And those are cumulative nominal under our baseline modeling assumptions.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

1:12

Dan Stickel

“in fiscal year 2061, which would be the first full fiscal year after the the second step up of the alternative volumetric tax. At that point in time, after adjusting for the inflation, there would be $212 million shared directly with the communities that the project resides in, an additional $285 million shared across the state based on population for community revenue sharing, and then the state at that point in time would get a little over $500 million.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

1:15

Bryce Edgmon

“the reason why I'm, I guess, at this juncture supportive of keeping in the 2028 timeline, if anything at all, it's just speaking of risk, poring through the Gaffney Klein document that was presented to the legislature in December 2025 that talks about all these sort of jurisdictions around the globe and the need for property tax relief and some sort of relief to get these very expensive front-end projects, gas line infrastructure, into place, is supported by years of analysis and efforts.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:42

Dan Stickel

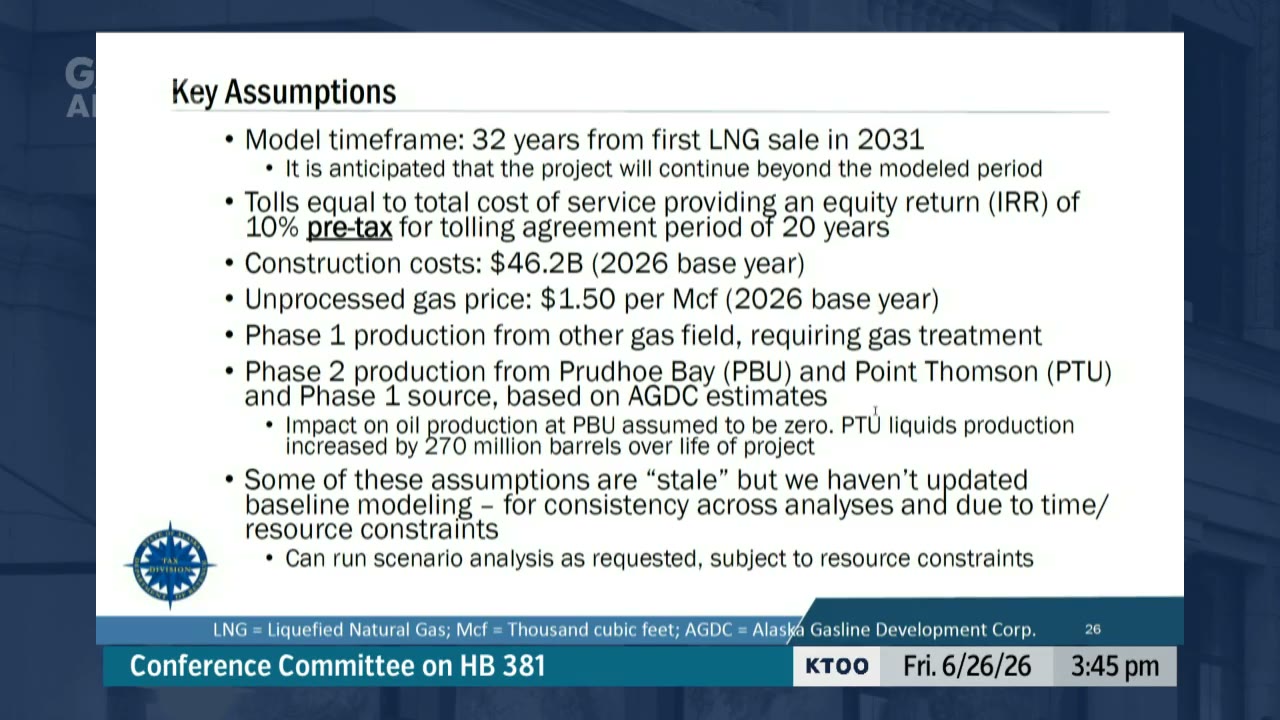

“Representative Ruffridge, through the chair, so that would be a great question to ask the developer, but based on the baseline assumptions that we have and the— what is in the futures market, it does look like a challenging project even with the tax relief.”Alaska Legislature: MSC2-20260626-1410

0:49

Matt Kissinger

“Representative Fields asked about these clawback mechanisms at that meeting, and what I said was, I said there, I said, and just to address this clearly, This is my words. And just to address this clearly, because I've heard many questions that dance around this, the clawback would be a paid clawback. And there's real important reason for that.”Alaska Legislature: MSC2-20260626-1410

0:33

Justin Ruffridge

“I think, Mr. Stickel, you're being generous when you say marginal. If the futures market is $8— and we're assuming a $1.50 upstream gas price and we're probably looking at the plus 20% line or the plus 40% line at— in real terms, none of the items I'm looking at on that screen seem to be even in the definition of marginal. It seems like they don't work.”Alaska Legislature: MSC2-20260626-1410

0:22

Dan Stickel

“Representative Ruffridge to the Chair, correct, yes. So the assumption is that there is significant capital expenditure for the Phase 2 and then kind of a steady-state operations beyond that. If the developer were to do a significant expansion, yes, that would reduce their corporate income tax liability.”Alaska Legislature: MSC2-20260626-1410

0:49

Dan Stickel

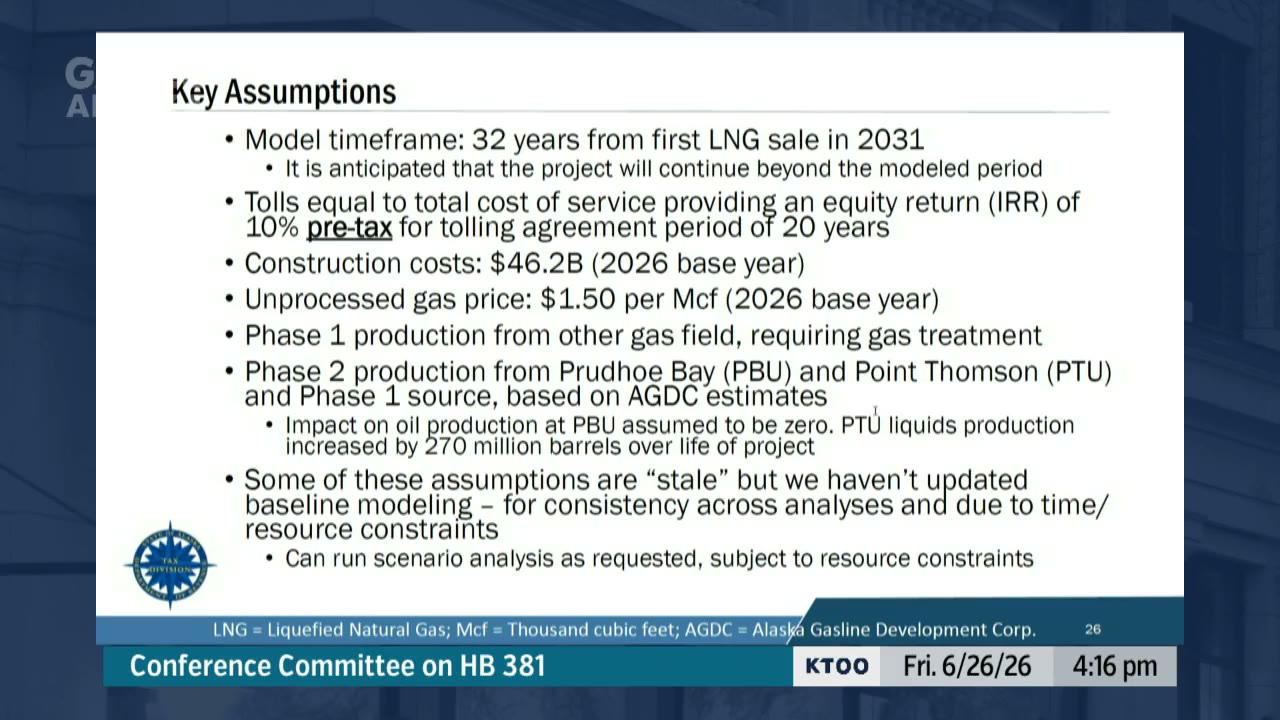

“a lot of these assumptions were developed before Glenfarn came onto the scene. We have not received a lot of detailed information and details details on project plan from them, given confidentiality. And so we have carried forward many of these assumptions. There was a significant amount of work that was done in 2018 and 2019.”Alaska Legislature: MSC2-20260626-1410

0:40

Justin Ruffridge

“I really would like to know how much the construction cost, because it seems to me to be a large assumption, weighs into what we're going to see here later, particularly on breakeven prices and other areas of, I think, importance to us as we're making decisions. If the construction cost is higher than what this model has assumed, what main areas does that affect in these following slides?”Alaska Legislature: MSC2-20260626-1410

0:43

Dan Stickel

“The act of agreeing on a new set of baseline assumptions, ideally that would be a months-long process where we would collaborate, we would review all of the latest information in detail, spend some time with it. We would collaborate with stakeholders, partners and agencies, developer, AGDC, industry, and kind of synthesize all of that information. And come up with a new set of baseline assumptions.”Alaska Legislature: MSC2-20260626-1410

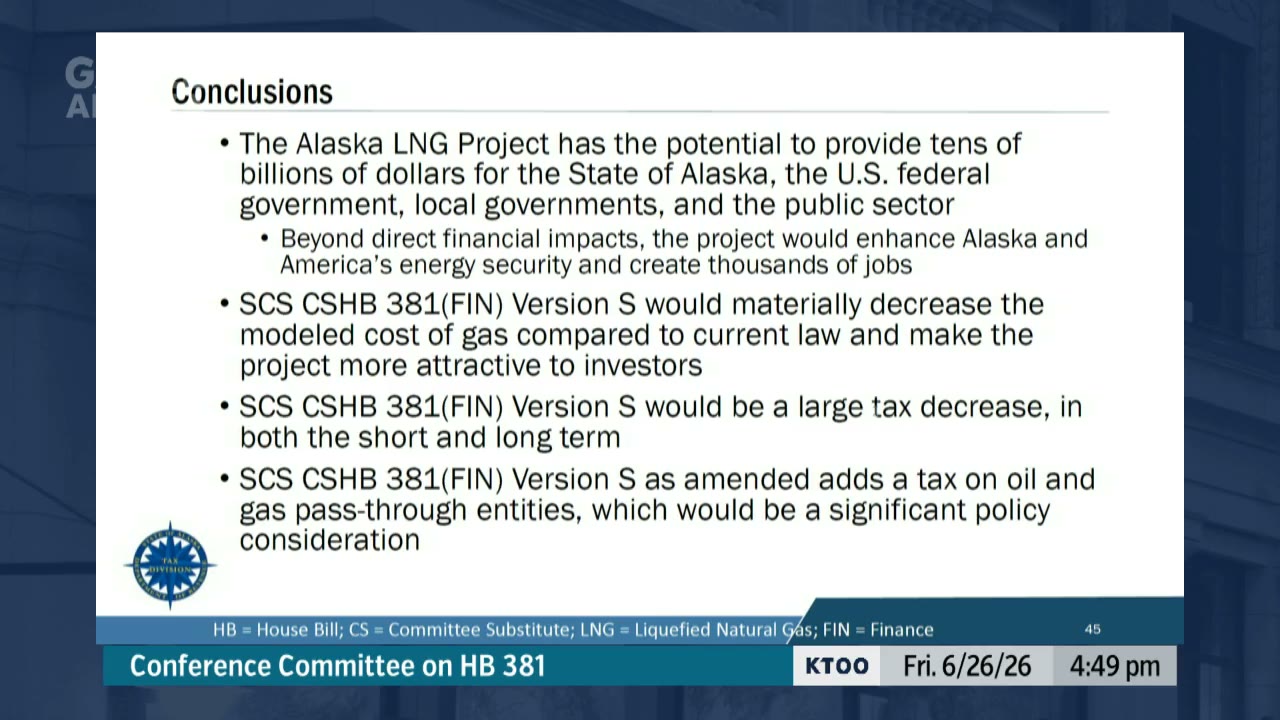

0:57

Dan Stickel

“The material impact between S and S as amended from a modeling standpoint is the inclusion of the pass-through entity tax.”Alaska Legislature: MSC2-20260626-1410

0:12

Bert Stedman

“they can draw erroneous conclusions from just reading that in isolation. And we've tried to ferret some of that out in our questions.”Alaska Legislature: MSC2-20260626-1410

0:30

Matt Kissinger

“If you're moving towards milestones and you're going to penalize your developer and they miss a milestone and you can just take everything away from them and they can lose everything, they will put nothing into it. And this is a $44 billion project that we're building. We need to put the very best work going into it. And that's why we're— there were these paid clawbacks with respect to our ability to push the developer out.”Alaska Legislature: MSC2-20260626-1410

0:29

Dan Stickel

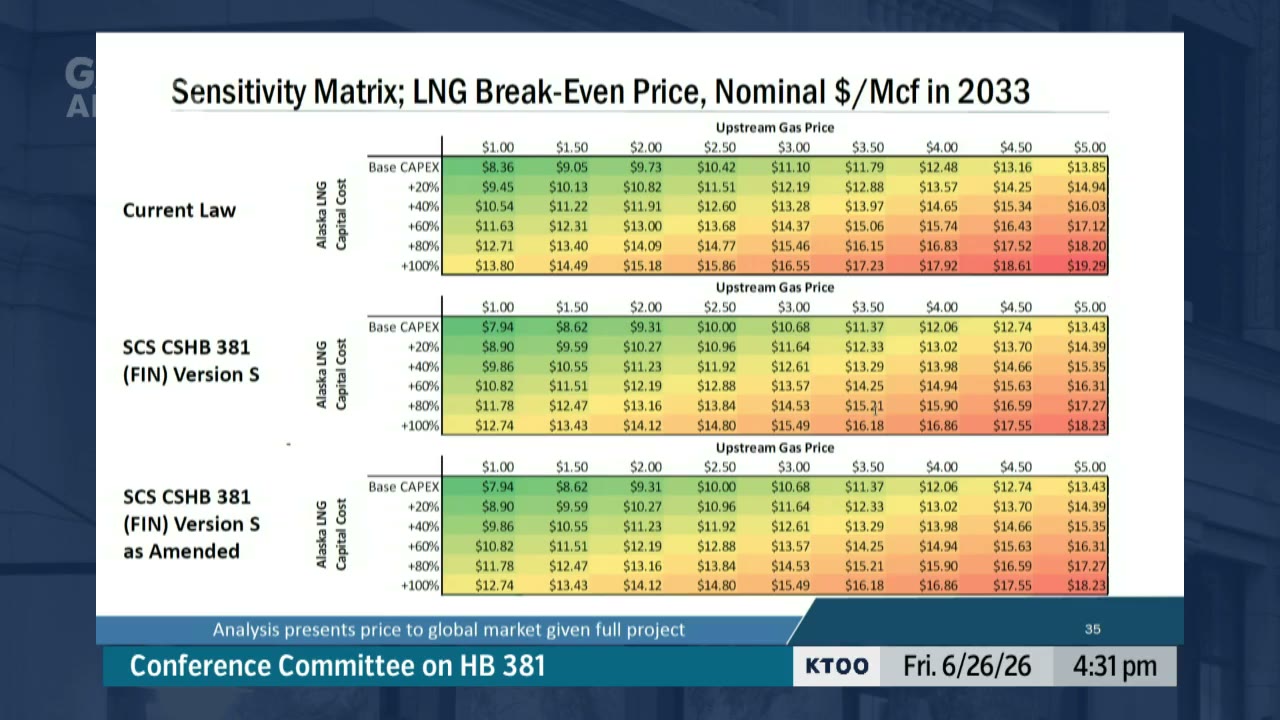

“broadly speaking, the various, you know, the various versions of the bill have kind of targeted that 50 cents or so reduction to that break-even cost of supply plus or minus 5 or 10 cents.”Alaska Legislature: MSC2-20260626-1410

0:24

Dan Stickel

“We note the significant policy difference between the two versions of the bill is that pass-through entity tax that is in the version that came out of the Senate floor. That does create— that does add a level of uncertainty uncertainty and is a significant policy decision for the committee to consider.”Alaska Legislature: MSC2-20260626-1410

0:36

Bert Stedman

“As far as it being a hypothetical potential of not going forward with the project, I don't believe it's that hypothetical because we've had numerous gas line projects that have not succeeded. This is just the latest one over the last 30 years. And there's a lot of FERC permits issued that never come to fruition.”Alaska Legislature: MSC2-20260626-1410

0:42

Dan Stickel

“The biggest one of these was the— that directly impacts the Department of Revenue was the implementation of the pass-through entity tax for oil and gas companies. This is a significant policy decision that's before the committee and the legislature.”Alaska Legislature: MSC2-20260626-1410

0:43

Dan Stickel

“The— with the alternative volumetric tax that reduces that breakeven price into the global market down to— from $9.05 down to $8.62 per 1,000 cubic feet.”Alaska Legislature: MSC2-20260626-1410

0:53

Dan Stickel

“the upstream and midstream would pay additional corporate income tax with the pass-through entity analysis. A portion of that would be an offset on federal tax because state taxes become a deduction against the federal tax. And then that would shift over life of project a little over— around $6 billion of cumulative revenue would shift from the companies and federal government to the state government.”Alaska Legislature: MSC2-20260626-1410