Dan Stickel

124:26 - 125:23

"The material impact between S and S as amended from a modeling standpoint is the inclusion of the pass-through entity tax."

“The material impact between S and S as amended from a modeling standpoint is the inclusion of the pass-through entity tax.”

- Speaker

- Dan Stickel

- Timestamp

- 124:26 – 125:23

- Community

- Alaska News

- Location

- Alaska

From the transcript

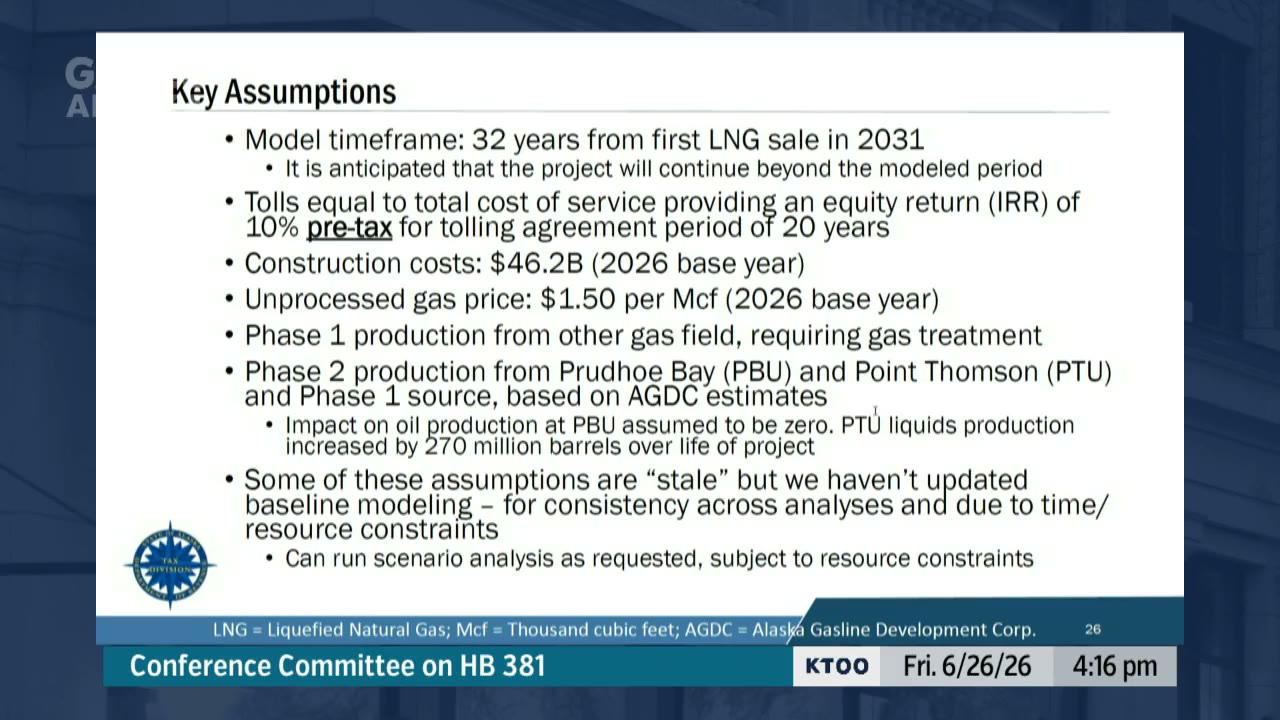

But that said, these are the assumptions that underlie the analysis that we are about to walk through. We do have some sensitivity analysis built into the presentation, and we are happy to run additional scenarios for the committee as we have for multiple committees going throughout this process. So slide 27, so for this slide— for this presentation we were asked to focus specifically on the Senate versions of the bill, specifically version S which came out of the Senate Finance Committee and then version S as amended which came off of the the floor. The material impact between S and S as amended from a modeling standpoint is the inclusion of the pass-through entity tax. In each of these scenarios, we show the impact if the full AKLNG project proceeds under each scenario.

Related Coverage

Alaska's gas-pipeline bill now carries a tax on Hilcorp and others

The Alaska Senate added a corporate income tax on oil and gas pass-through entities like Hilcorp to the AK LNG gas-pipeline bill (HB 381), effective 2028 regardless of the project.

State economist: even with tax breaks, the gas line barely works

State economist Dan Stickel told a legislative conference committee Friday that the Senate version of HB 381 reduces the Alaska LNG export break-even price from $9.05 to $8.62 per thousand cubic feet — still above current futures market prices near $8 — prompting Rep. Justin Ruffridge to say the project simply "doesn't work."