Video Clips

Quoted moments from Alaska public meetings, hearings, and press conferences.

Clips from Alaska Department of RevenueClear

0:17

Dan Stickel

“It does start with the same effective tax rates as the House version and simply fixes those rates and allocations in, in statute. The Senate version then added in the two doublings of the tax rate that was a major change from the House version.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:21

Dan Stickel

“The first effective 10 years, after 10 years of LNG export operations, where the tax rate doubles. And then the second effective in 2060, where the tax rate doubles. Again.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:22

Mike Cronk

“if we do nothing, these numbers go away, we have nothing here. There's zero revenue brought to this state. There's zero revenue brought to many communities.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:58

Bryce Edgmon

“I feel like I think if FID isn't, for Phase 1, arrived at by 2028, there's justification for this issue to come back before the legislature to have a longer runway to engage in this discussion. I would submit to you or anyone else that we should not have gotten this bill on March 20th. We should have gotten this a lot earlier so we could, to pour over this in a way that complies with all the sort of what-if scenarios that are out there and also to be maybe a better partner to you as a developer overall to get our work done in a longer frame of time. So I guess at this point I'm not convinced that removing that 2028 FID deadline— and remember, it's just for Phase 1, it's not for Phase 2. You know, I don't know that it serves our best interests”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:25

Dan Stickel

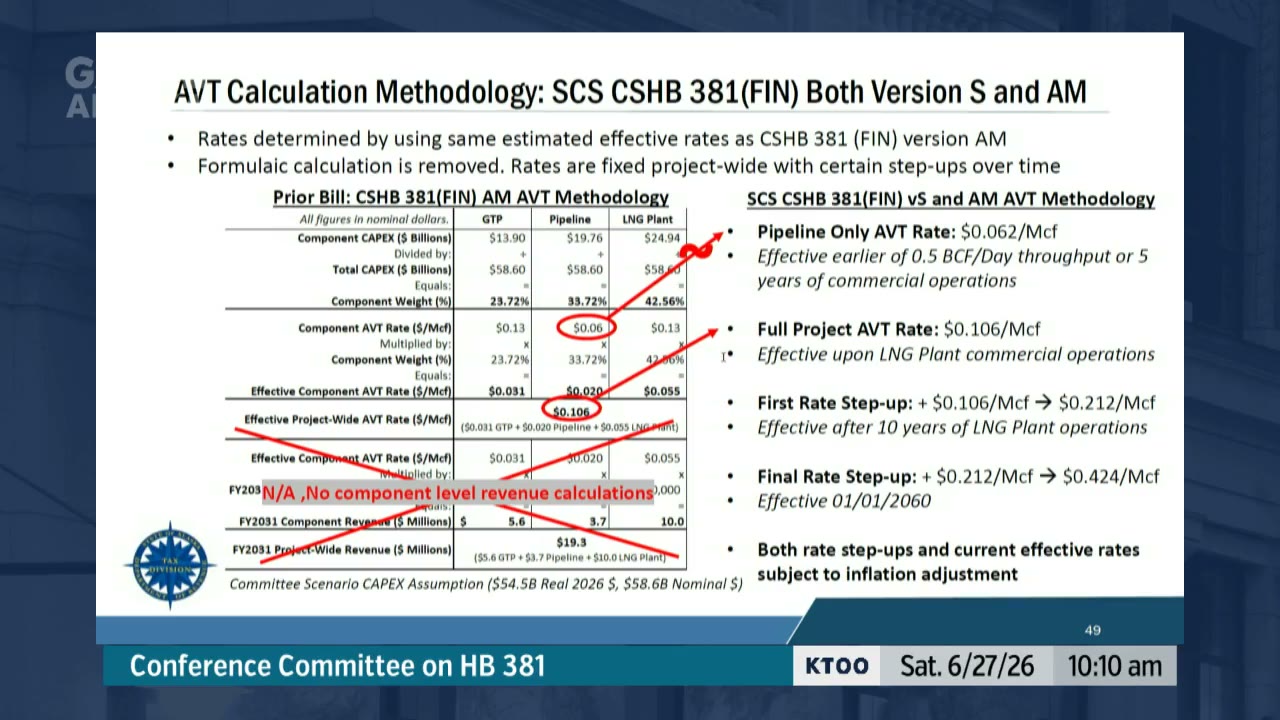

“fixing the percentages does increase some of the certainty and makes it easier to calculate and plan. Removes one item of potential contention going forward.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:26

Adam Prestidge

“That penalty is— would be losing the tax— the tax treatment of the project. The result of that would be at the front end, investors would look at this as additional risk, And they would have to price in that risk into how they invest in the project. And so the ultimate outcome of this would be making the project more expensive and require more investment capital.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:34

Lyman Hoffman

“On the first bullet point where the Senate version removes the calculation complexities, does the department have an opinion on that? Especially since it has the same effective rate as the House version simplification, does that reduce the amount of work to the department.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

1:12

Dan Stickel

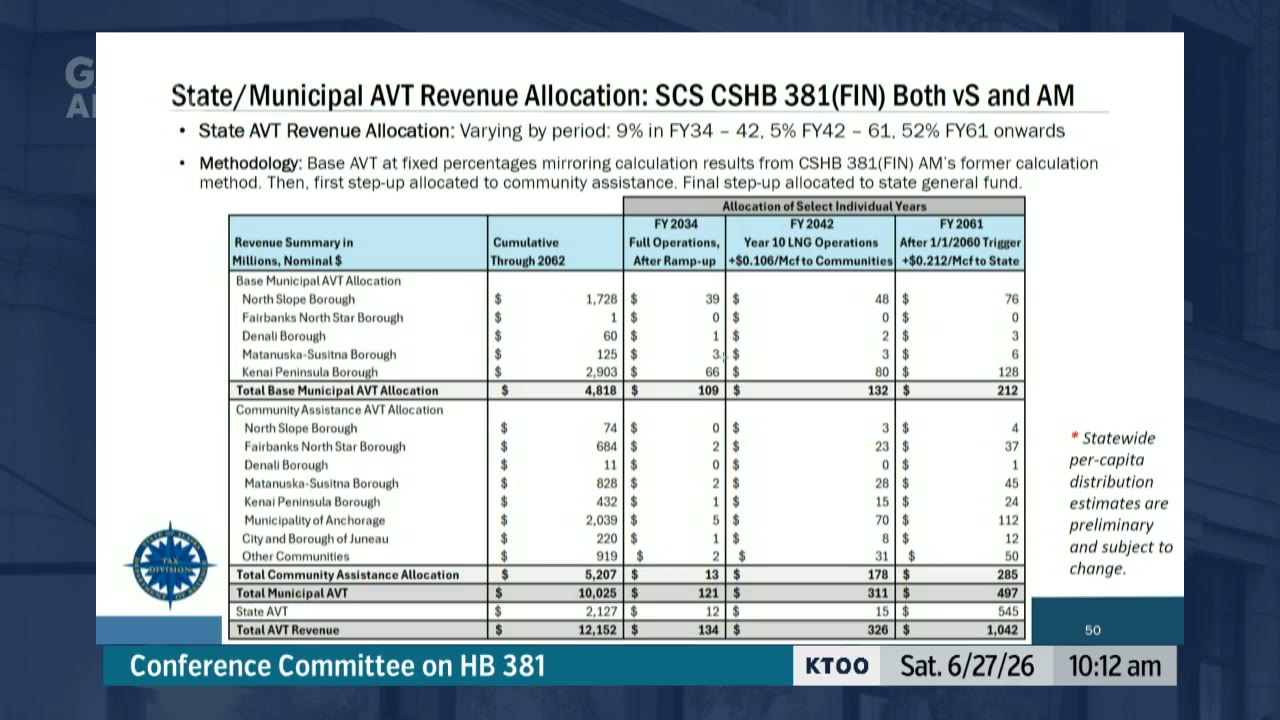

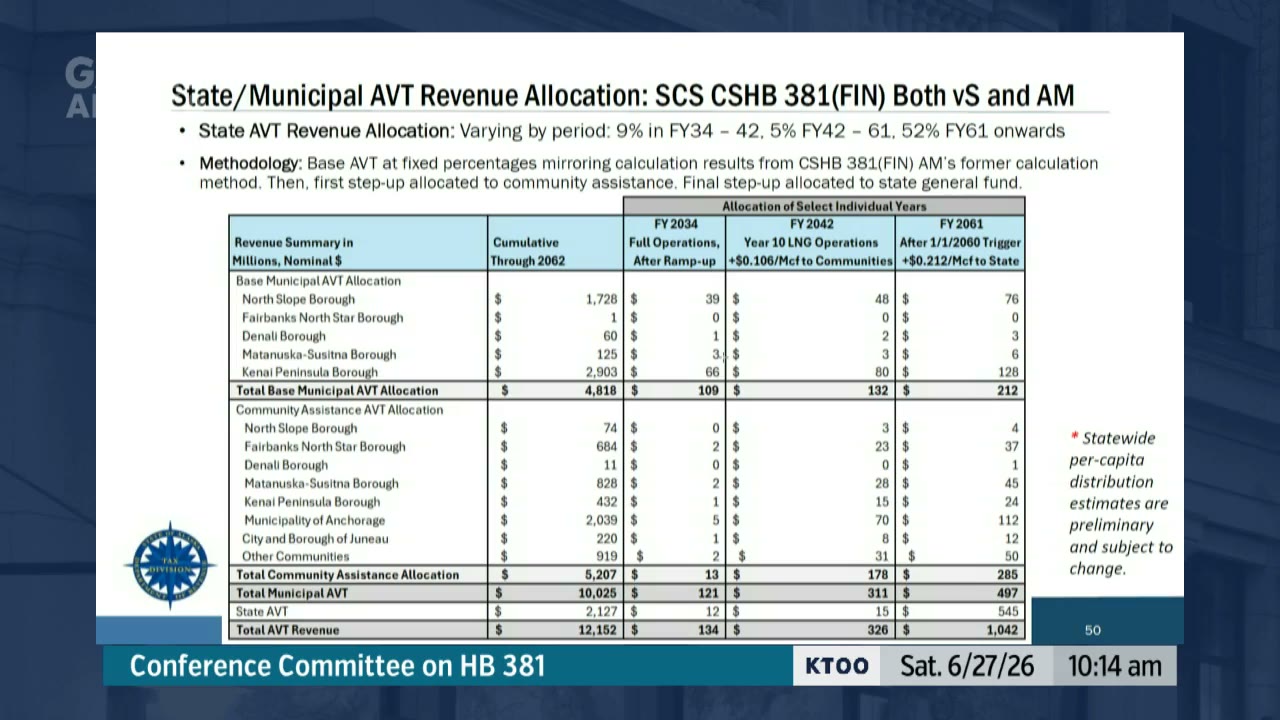

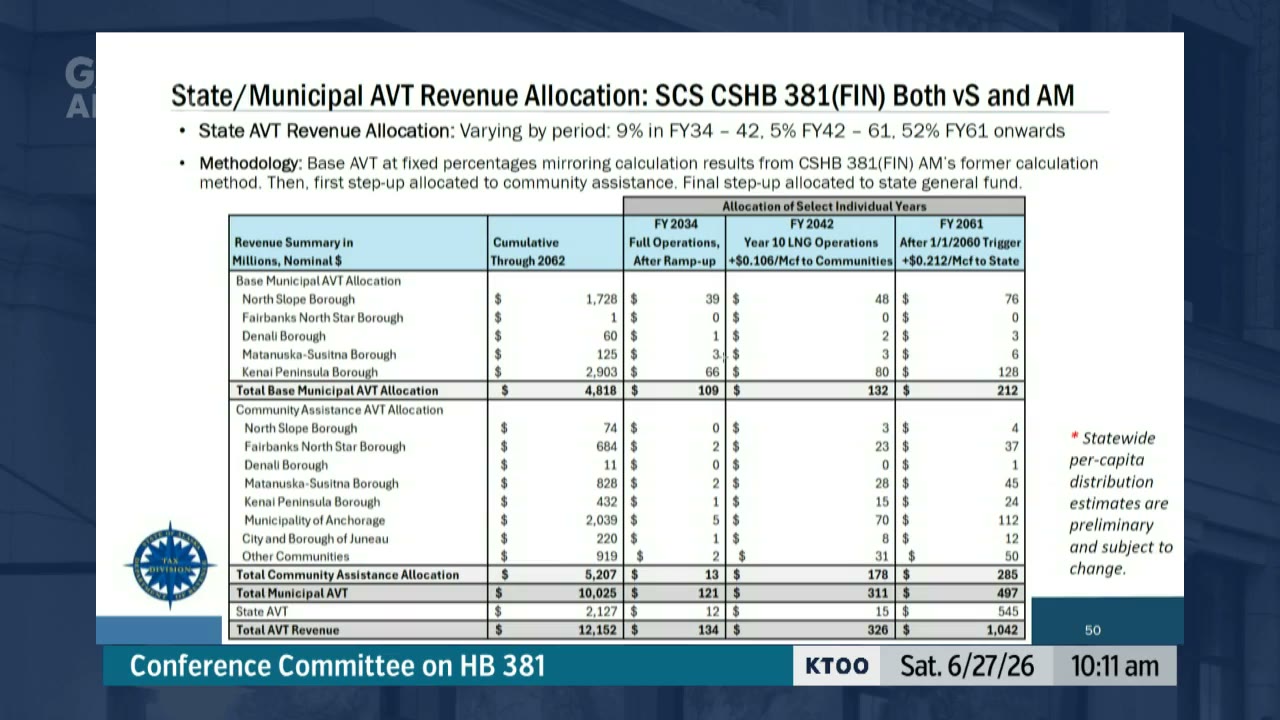

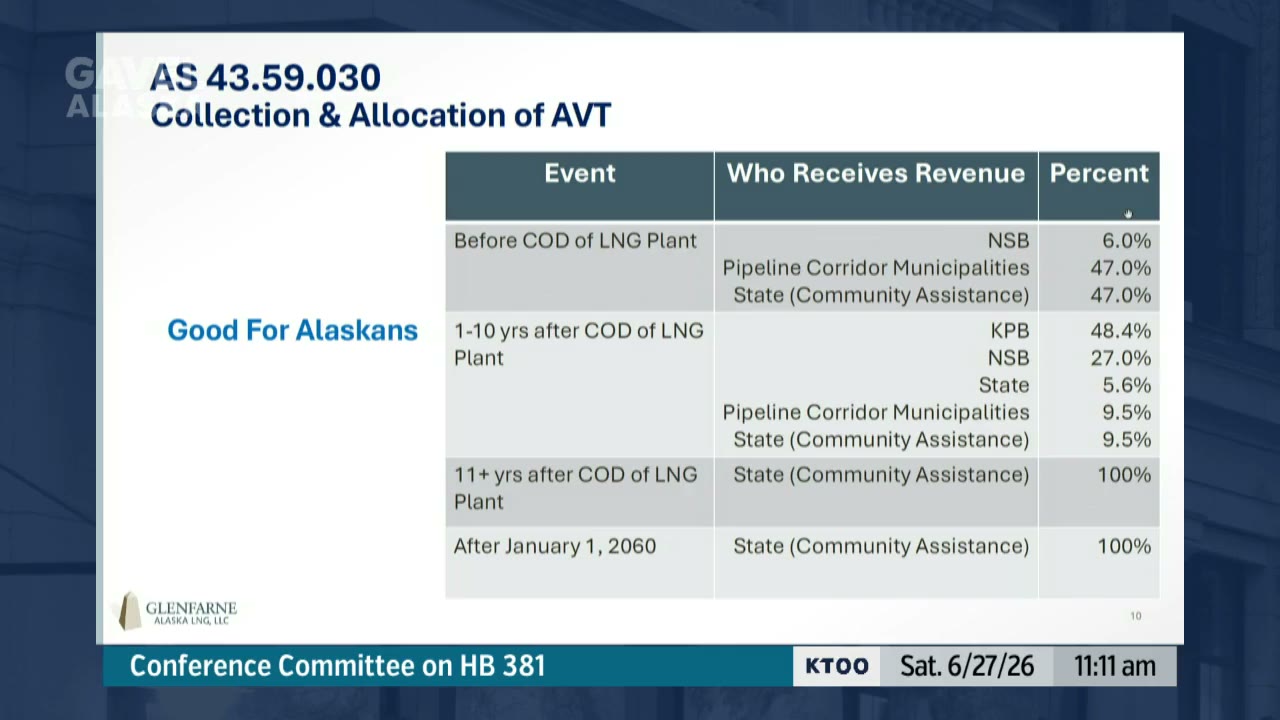

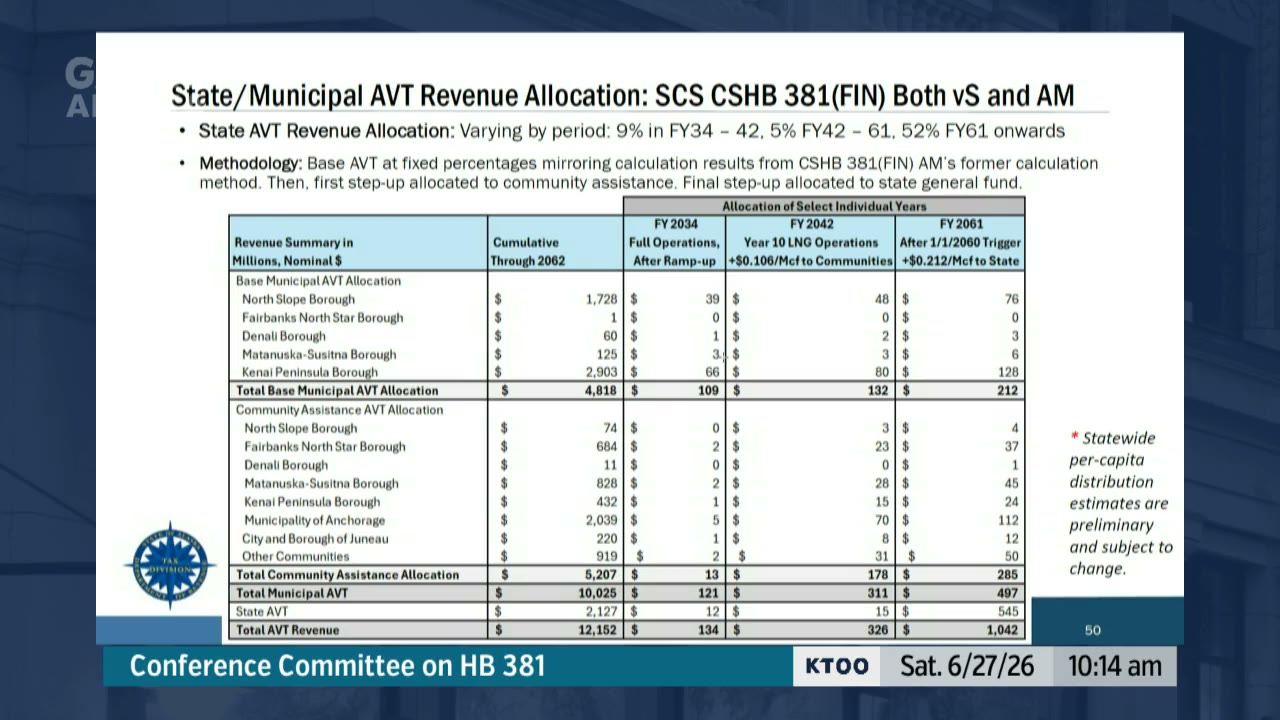

“in fiscal year 2061, which would be the first full fiscal year after the the second step up of the alternative volumetric tax. At that point in time, after adjusting for the inflation, there would be $212 million shared directly with the communities that the project resides in, an additional $285 million shared across the state based on population for community revenue sharing, and then the state at that point in time would get a little over $500 million.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:38

Dan Stickel

“the state starts out receiving about 9% of the AVT revenue. That will drop to 5% with the first doubling of the tax rate.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

1:08

Dan Stickel

“in those early years, the vast majority of the revenue is allocated to the communities that the project is directly in. So $109 million of the AVT in 2034 would go to those 5 municipalities, with an additional $13 million spread statewide to community revenue sharing and $12 million to the state. And then the second column shows after the first step up in the alternative volumetric tax, and that additional step up goes entirely to community revenue sharing.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

1:01

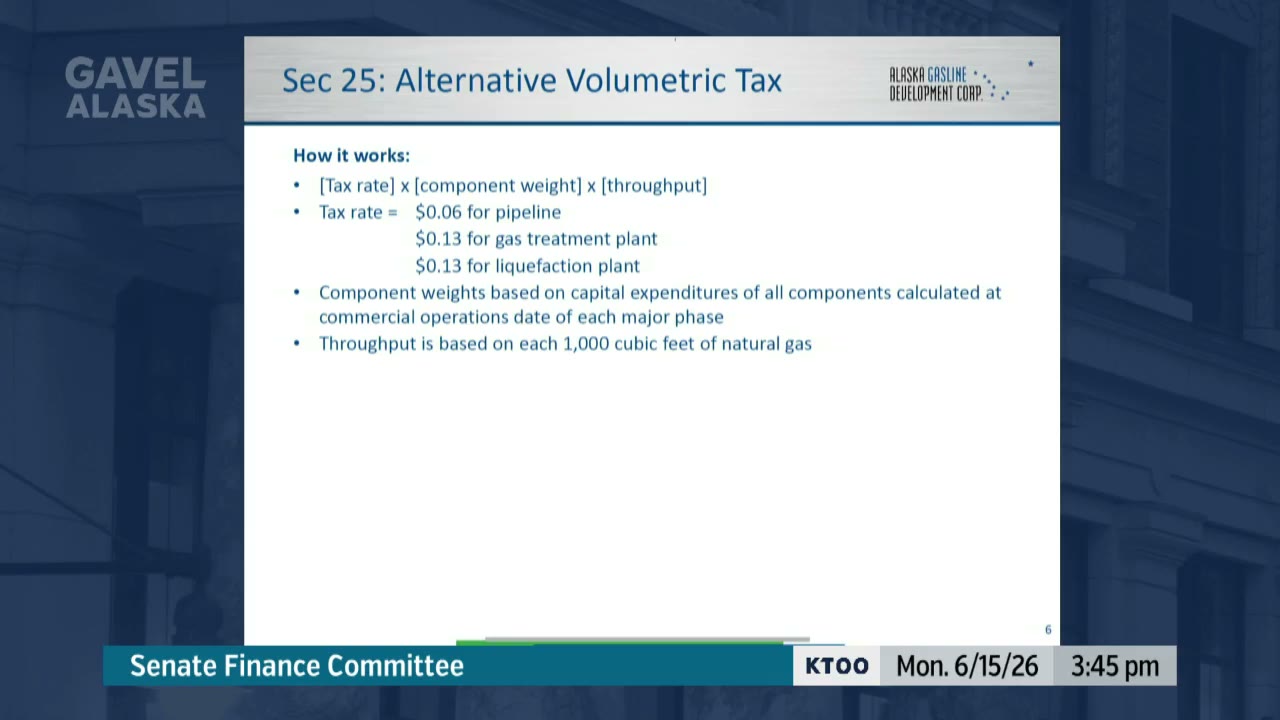

Dan Stickel

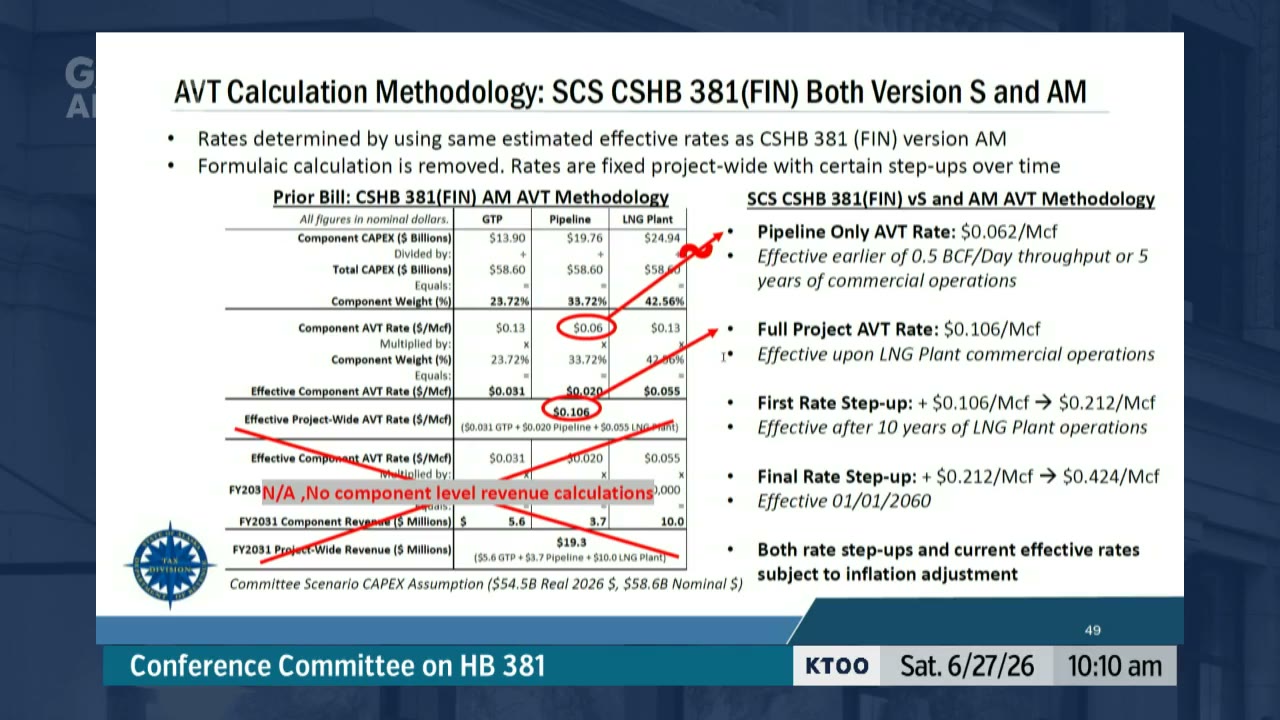

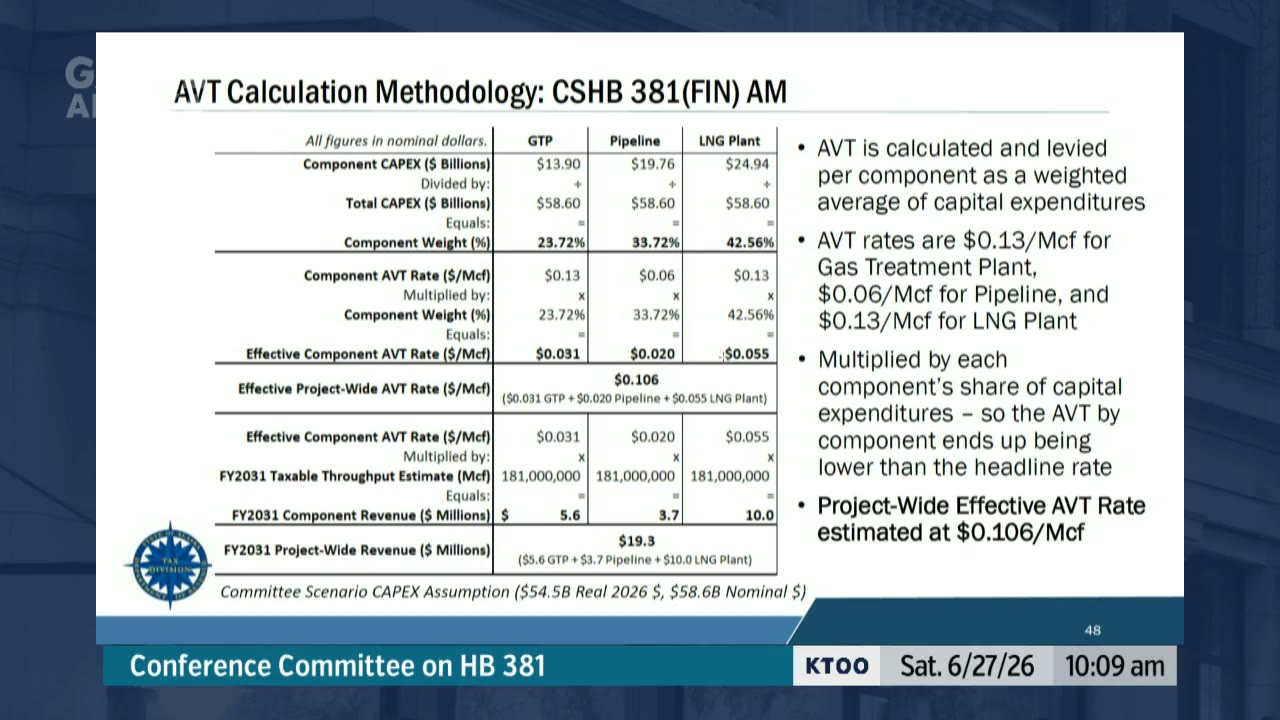

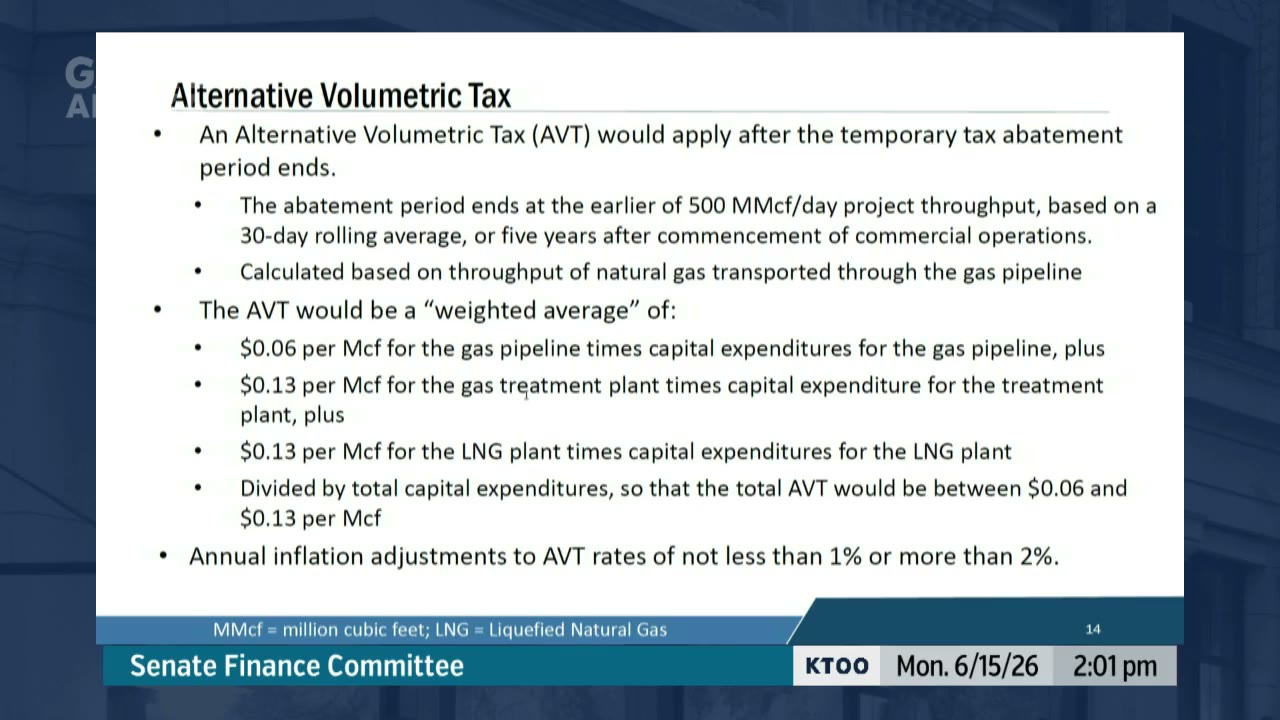

“they moved away from this weighted average approach and instead just put in the flat rates for each component of the project. So they took that about 6 cents per MCF rate on the pipeline component and made that a 6.2 cents per 1,000 cubic feet tax rate for phase 1 of the project. And then they took that 10.6 cents per thousand cubic feet weighted average with the capital expenditures weighting and just made that the tax rate once LNG exports began.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

1:14

Dan Stickel

“under the House version of the bill, the alternative volumetric tax was calculated and levied on a per-component basis as a— using a weighted average of capital expenditures. And so once the full project was complete, we would look at the, the total capital expenditures that were spent on each component of the project, being the treatment plant, the pipeline, and the LNG export facility.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:32

Dan Stickel

“the capital expenditure weighting and the project component weighting, that applied both for calculating the initial tax rates, but then also applied for calculating the sharing out to municipalities. And that sharing out to municipalities has also been fixed in statute. In the Senate version of the bill. So removing some of that complexity. The other addition that the Senate made is the two step-ups.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:24

Dan Stickel

“for a pipeline-only portion of the project, you'd have a 6-cent per MCF tax rate, and then once the full project was in operations, we would estimate that the tax rate on a weighted average basis would be about 10.6 cents per 1,000 cubic feet.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:30

Adam Prestidge

“we as the project developer at 8 Star have no objection to the 2028 FID deadline. We're only raising concerns around the 2032 completion of construction deadline.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

1:15

Bryce Edgmon

“the reason why I'm, I guess, at this juncture supportive of keeping in the 2028 timeline, if anything at all, it's just speaking of risk, poring through the Gaffney Klein document that was presented to the legislature in December 2025 that talks about all these sort of jurisdictions around the globe and the need for property tax relief and some sort of relief to get these very expensive front-end projects, gas line infrastructure, into place, is supported by years of analysis and efforts.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

1:12

Adam Prestidge

“our practical expectation is that we will complete the project ahead of these timelines, and so the deadline or the timeline that you said The end of the year for FID maintains— continues to be our target. And we would— if we were to follow a target construction schedule, even with some delays, we would complete the project before December 31st, well before December 31st, 2032.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:55

Adam Prestidge

“The 2032 completion of construction is more about managing theoretical risk that lenders and investors will look at when they make an investment decision on the project. And so regardless of how we all want to move fast, Regardless of the timing around the energy availability out of the Cook Inlet, lenders and investors will just see this numerically and assign it a hypothetical risk that will make the project more expensive. And so we don't see it adding any additional incentive that isn't there already. It just adds risk to the project that will be priced into the financing.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:27

Adam Prestidge

“The deadline of 2037 is well within— well beyond the project completion deadline, even if we put a couple years of contingency on that. And so a 2037 deadline doesn't have that same risk profile to the FID investors. And so for that reason, we suggest deleting the 2032 deadline.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:12

Bert Stedman

“I think after January 1st, 60, 100% goes to the general fund, not community assistance. Is that right?”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:34

Dan Stickel

“In the version that passed the House, our break-even price was $8.57 under our baseline scenarios for gas delivered into the global market. Under the version that passed the Senate, it was $8.62 per 1,000 cubic feet. So a 5 cents per 1,000 cubic feet increase from the House version to the Senate version.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:19

Dan Stickel

“total state benefits under our baseline model assumptions, which which we talked about yesterday, through 2042 would be $7.5 billion to the state.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:28

Dan Stickel

“through 2062, which is the to the extent of our modeling, $32.2 billion to the state. And those are cumulative nominal under our baseline modeling assumptions.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:05

Dan Stickel

“But then increase to 52% of the total AVT with the second doubling of the tax rate.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

1:02

Adam Prestidge

“the 2028 deadline, it puts a bit of a risk on the developer and it puts an incentive on the developer, but it does that at a time before billions of construction dollars have been put at risk on the project. And so essentially putting that 2032 deadline puts additional risk on all the investment dollars that doesn't serve the benefit of actually accelerating anything. And the issue that then comes up is if there were a delay in construction, if there were litigation, if there was COVID, you know, an epidemic, that's just, those are all hypothetical risks that could occur, that have occurred on other projects, that lenders and investors are going to be nervous about.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:13

Dan Stickel

“for the first doubling of the tax rate, 100% of that doubling would go to community assistance, and then for the second doubling of the tax rate, 100% of that that next doubling would go to the state unrestricted general fund.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:21

Dan Stickel

“the Senate version of the bill removes some of the complexity in the calculation that was in the prior version of the bill.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:53

Dan Stickel

“it's a 20 mils tax or 2% of assessed value, and that assessment is done centralized by the State Department of Revenue. We manage the appraisal and assessment process for all oil and gas property in the state, and then any municipal oil and gas property taxes are allowed as a credit against that state tax.”Alaska Legislature: Senate Finance - June 15, 2026 1:30pm · Jun 15, 2026

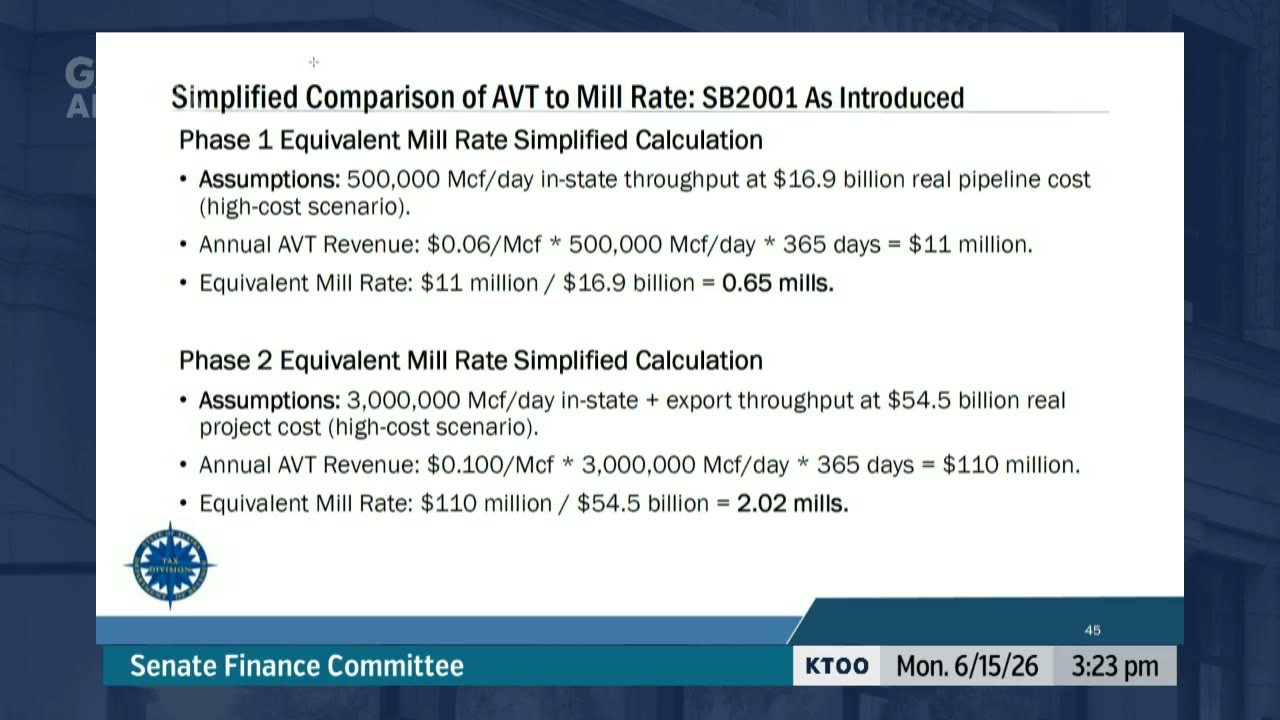

0:20

Dan Stickel

“each additional mil of equivalent mil rate on the full project would be equivalent to about 5 cents of AVT revenue.”Alaska Legislature: Senate Finance - June 15, 2026 1:30pm · Jun 15, 2026

0:42

Bert Stedman

“I don't want to get personally lost into big dollars if the whole project is built and it's full of gas and everything's wonderful. I think we should be concentrating on the economic of the project and trying to see how close we are to the hurdle rate to get it to FID or not.”Alaska Legislature: Senate Finance - June 15, 2026 1:30pm · Jun 15, 2026

0:20

Jesse Kiehl

“through some of my history, both here in the Capitol and in municipal government, it's pretty good we know what it means is never good enough on tax law. You have to have the words on the paper.”Alaska Legislature: Senate Finance - June 15, 2026 1:30pm · Jun 15, 2026

0:34

Dan Stickel

“we calculate based on our, our assumptions that the effective rate would be somewhere between 10 and 11 cents per 1,000 cubic feet.”Alaska Legislature: Senate Finance - June 15, 2026 1:30pm · Jun 15, 2026

0:43

Dan Stickel

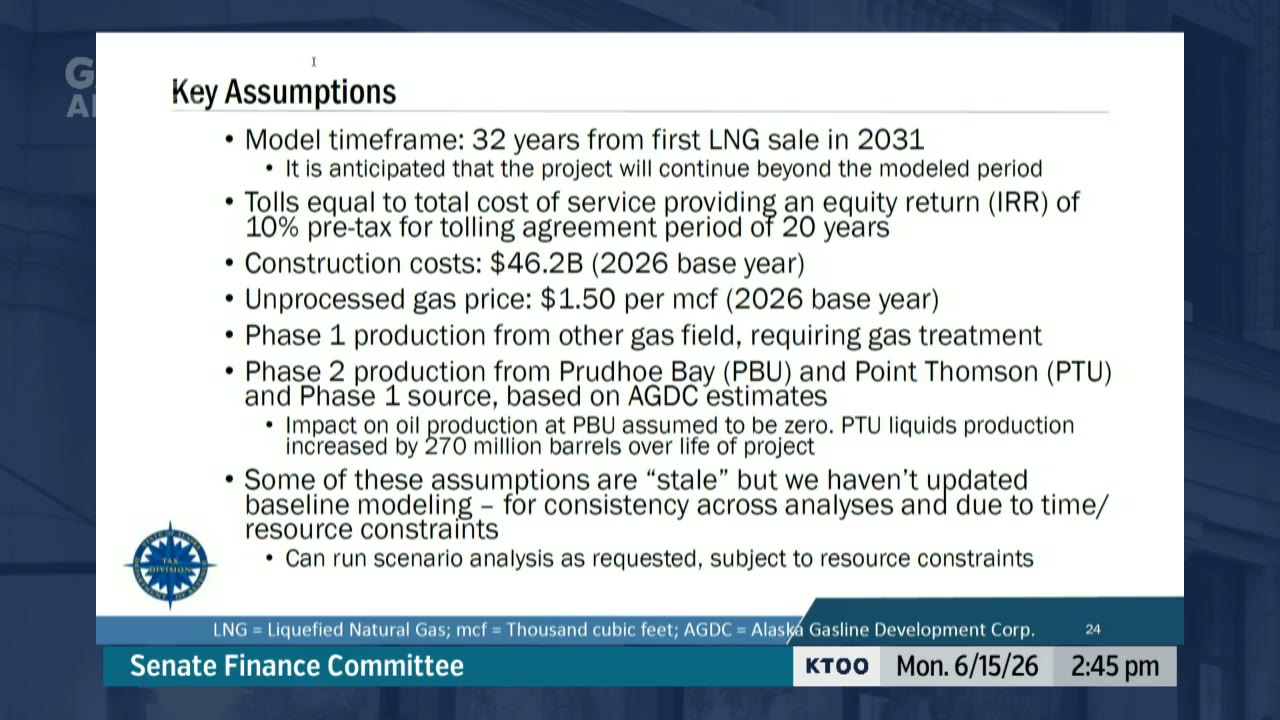

“given the time and resource constraints with a special session that ends in 4 days, we have maintained our baseline model assumptions at this point.”Alaska Legislature: Senate Finance - June 15, 2026 1:30pm · Jun 15, 2026

0:57

Dan Stickel

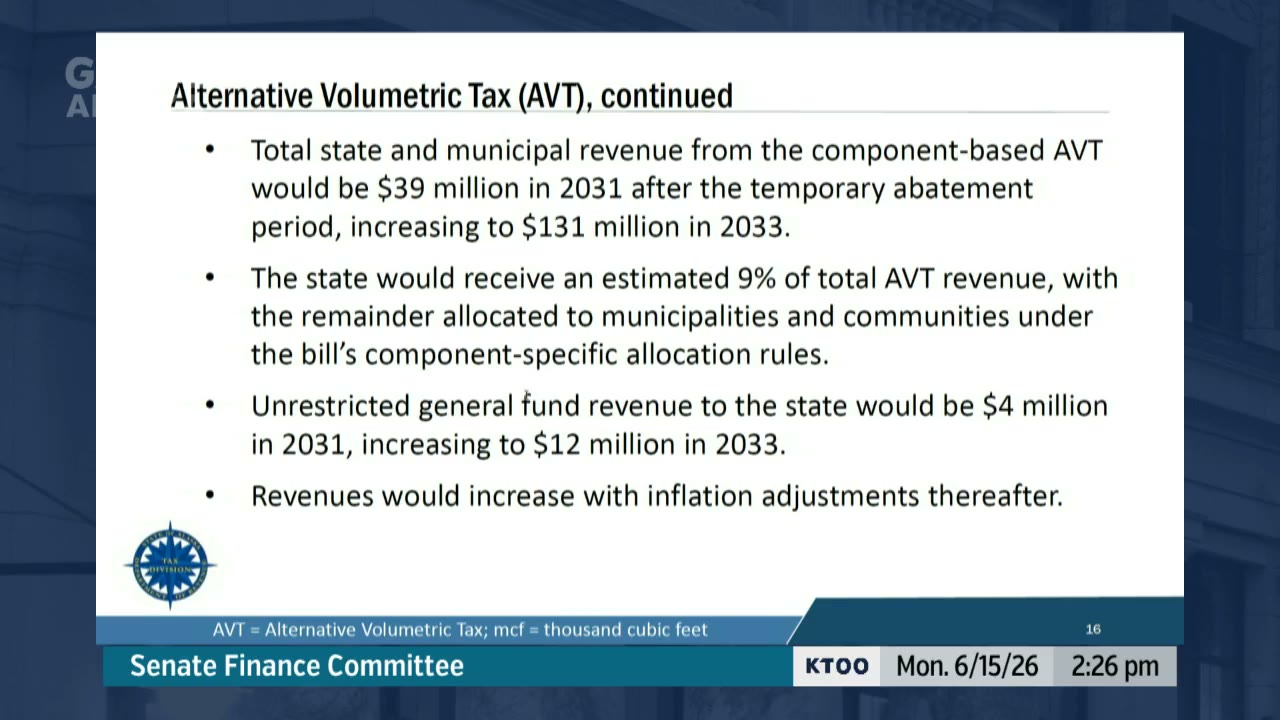

“we look at, under our baseline modeling, 2031 is the first year of exports when the first train comes online, and that would be the first year of tax liability for the alternative volumetric tax with a total of $39 million paid in, and that would increase to $131 million by 2033, which would be the first year of the full export operations. Under this version of the bill, the state would receive about 9% of the total AVT revenue, with the remainder allocated to the various municipalities and communities as outlined in this bill.”Alaska Legislature: Senate Finance - June 15, 2026 1:30pm · Jun 15, 2026

0:55

Bert Stedman

“The issue at the table is the gas line. And what would be nice if we could see an analysis on the gas line itself and also the marginal impact of the change in property tax from the 20 mills to, you know, the— to the 2 mills, which is basically what's on the table.”Alaska Legislature: Senate Finance - June 15, 2026 1:30pm · Jun 15, 2026

0:28

Bert Stedman

“I'm kind of curious when the corporate income tax kick in on the gas line. You know, I think it's somewhere around 20, 21 years out, which means it's time you deal with your depreciation and your interest costs and your carry-forwards. It's not making any money for decades.”Alaska Legislature: Senate Finance - June 15, 2026 1:30pm · Jun 15, 2026

0:21

Bert Stedman

“I'd like to know the operating expense of the pipeline. I'd like to know the operating expense of the liquefaction plant, um, and some of these other component parts, um, that you have to plug in your model.”Alaska Legislature: Senate Finance - June 15, 2026 1:30pm · Jun 15, 2026

0:40

Bert Stedman

“if nothing else for us to, you know, nice to have a hearing on it, but to take a look at it, I think it's critical that we know if we give a concession with our left hand, it's not taken away with some mechanism on the right hand. And how much of a concession is needed to get it to the economic hurdle? And maybe it's zero tax, for all I know. But I think we need to see that on Phase 1, because that's what they're trying to get the FID on, is my understanding.”Alaska Legislature: Senate Finance - June 15, 2026 1:30pm · Jun 15, 2026

0:18

Bert Stedman

“I'd like to know the marginal impact of a 1 millage rate change. You got 2.13 mills here. If you change that assumption in your model to make that 3.13 mills, what's the effect of the economics of the project?”Alaska Legislature: Senate Finance - June 15, 2026 1:30pm · Jun 15, 2026

0:08

Bert Stedman

“I think the model has all that. It's got to have all that data in there to just print it out. It doesn't have to be fancy looking.”Alaska Legislature: Senate Finance - June 15, 2026 1:30pm · Jun 15, 2026

0:19

Bert Stedman

“We can't control capital cost or operating costs. Or much other variables. We have very few levers we can move. But we can make that 1 mil equivalent, 2 mil equivalent, 3 mil, 4 mil, 5 mil, whatever we want.”Alaska Legislature: Senate Finance - June 15, 2026 1:30pm · Jun 15, 2026

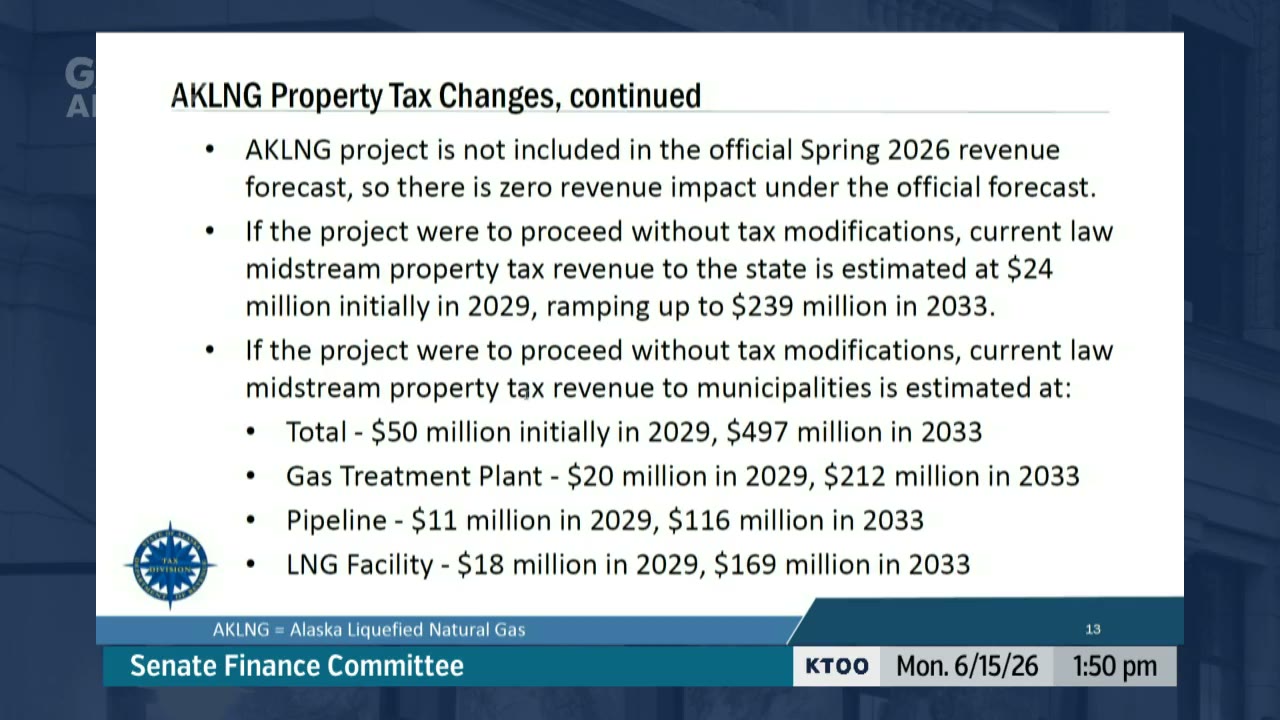

1:14

Dan Stickel

“Property tax revenue to the state would be estimated at $24 million initially in 2029, ramping up to $239 million by 2033, which is when the full export operations begin and the project construction is completed. And then the municipal revenues, in addition to those state revenues, would start at $50 million initially in 2029, ramping up to $497 million in 2033. So all told, you have a little over $700 million per year of property tax revenue that would come just from the AK LNG project to the state and municipalities if the project were to proceed under current law.”Alaska Legislature: Senate Finance - June 15, 2026 1:30pm · Jun 15, 2026

0:46

Adam Prestidge

“this tax structure, the alternative volumetric tax, has the benefit of creating alignment. And so the more, the more gas that flows on the pipeline, the greater the revenue to, to the state. The more gas that flows on the pipeline, the lower the cost of gas to the ratepayers.”Alaska Legislature: Senate Finance - June 15, 2026 1:30pm · Jun 15, 2026

0:22

Bert Stedman

“isn't there a timing difference between when the $0.16 was agreed to and when the concept of the volumetric tax numerics were put in play, like a couple of months difference in time?”Alaska Legislature: Senate Finance - June 15, 2026 1:30pm · Jun 15, 2026

0:15

Bert Stedman

“I think there's a couple months difference in when the 16 cents was in play and when the concept of the effective 2 mil tax rate was put on the table or put in play.”Alaska Legislature: Senate Finance - June 15, 2026 1:30pm · Jun 15, 2026

1:08

Bert Stedman

“I think 2 mils of our 2% of $16 billion is somewhere around $320 million. So I just need to, I guess, get some of these numbers adjusted. And I'd rather, Mr. Chairman, have us look at the aggregate dollars and going to the state, and then if there's a split to the municipalities like we do with our oil tax, we look at the whole, you know, the portion that goes to each borough and then a portion that goes to the state. But if we don't use the aggregate dollar amount, we get our tax modeling off.”Alaska Legislature: Senate Finance - June 15, 2026 1:30pm · Jun 15, 2026

0:29

Bert Stedman

“Frankly, when I look at this bill and I see 2 mills, I find that alarmingly low. If I could pay 2 meals for my house, I'd run down to City Hall with a Christmas card to the mayor.”Alaska Legislature: Senate Finance - June 15, 2026 1:30pm · Jun 15, 2026

0:44

Bert Stedman

“what we're being asked for is concessions, and I want to know what we actually gain, whatever concession we give, not looking at hypotheticals 30 years out. We're trying to get a financing package across the line, is my understanding. Otherwise, why would we give a concession?”Alaska Legislature: Senate Finance - June 15, 2026 1:30pm · Jun 15, 2026