Video Clips

Quoted moments from Alaska public meetings, hearings, and press conferences.

Clips from Alaska Gasline Development CorporationClear

0:38

Dan Stickel

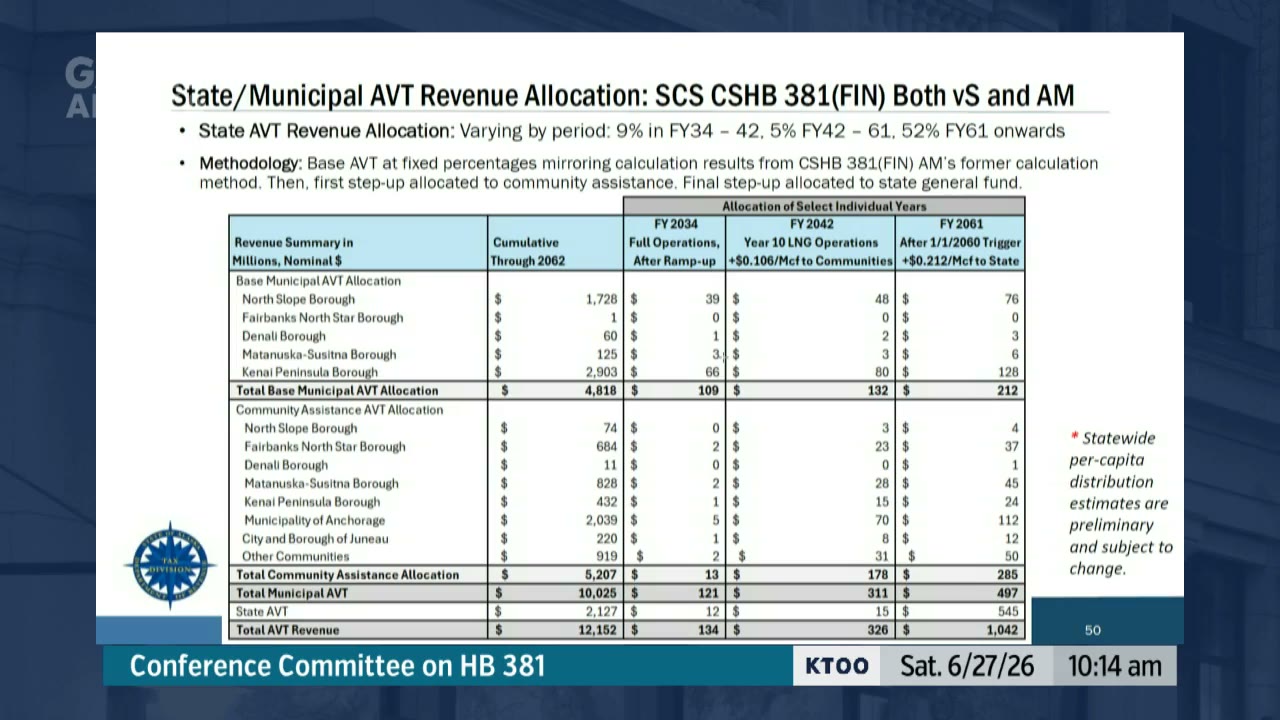

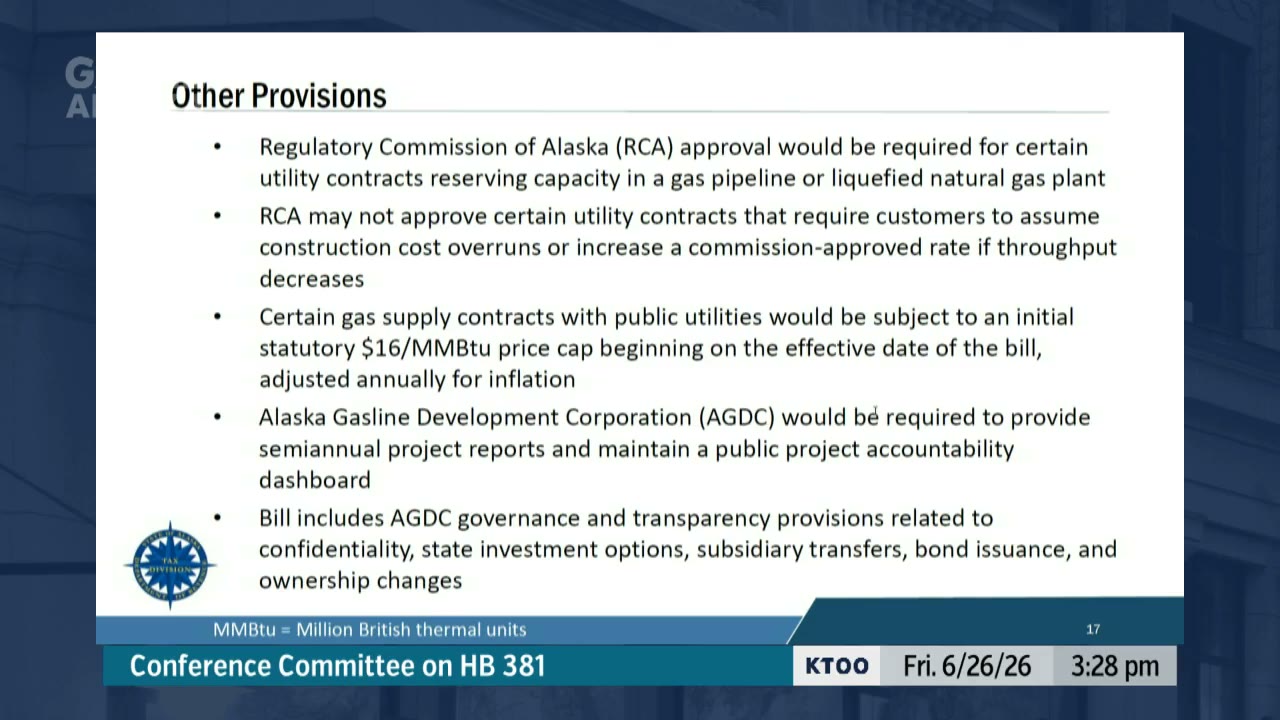

“the state starts out receiving about 9% of the AVT revenue. That will drop to 5% with the first doubling of the tax rate.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:22

Mike Cronk

“if we do nothing, these numbers go away, we have nothing here. There's zero revenue brought to this state. There's zero revenue brought to many communities.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:17

Dan Stickel

“It does start with the same effective tax rates as the House version and simply fixes those rates and allocations in, in statute. The Senate version then added in the two doublings of the tax rate that was a major change from the House version.”Alaska Legislature: Joint Conference on HB381, 6/27/26, 10am · Jun 27, 2026

0:38

Dan Stickel

“we've heard from some impacted taxpayers that the top end of the range may be an aggressive assumption. And so we continue to present this as a range.”Alaska Legislature: MSC2-20260626-1410

0:22

Dan Stickel

“Representative Ruffridge to the Chair, correct, yes. So the assumption is that there is significant capital expenditure for the Phase 2 and then kind of a steady-state operations beyond that. If the developer were to do a significant expansion, yes, that would reduce their corporate income tax liability.”Alaska Legislature: MSC2-20260626-1410

0:57

Dan Stickel

“The material impact between S and S as amended from a modeling standpoint is the inclusion of the pass-through entity tax.”Alaska Legislature: MSC2-20260626-1410

0:22

Matt Kissinger

“Senator Steadman, through the chair, if you would be willing to provide us with a copy of that document, then we can consider redacting it and reviewing it. But as of now, we've only been able to look at that document. We don't have, uh, we don't have our own copy of that.”Alaska Legislature: MSC2-20260626-1410

0:32

Adam Prestidge

“this is a mechanism that is only exercisable at the state's option. In terms of Glenfarn's ability to seek recourse or any kind of compensation, we don't have that mechanism. We can't ask the state to exercise this option. If Glenfarn decides to abandon the project, we do so with no recourse.”Alaska Legislature: MSC2-20260626-1410

0:30

Matt Kissinger

“If you're moving towards milestones and you're going to penalize your developer and they miss a milestone and you can just take everything away from them and they can lose everything, they will put nothing into it. And this is a $44 billion project that we're building. We need to put the very best work going into it. And that's why we're— there were these paid clawbacks with respect to our ability to push the developer out.”Alaska Legislature: MSC2-20260626-1410

0:19

Calvin Schrage

“One question that I would have, which has not been addressed as of yet, is who is able to claim value for any tax abatement that's provided by the legislature. I think I've not heard that issue addressed yet and would appreciate hearing from you on that.”Alaska Legislature: MSC2-20260626-1410

0:11

Bert Stedman

“I think the buyback is one of them. There's mechanics if you take a literal interpretation of that document, it may not be as accurate as looking at it in the entirety.”Alaska Legislature: MSC2-20260626-1410

0:43

Dan Stickel

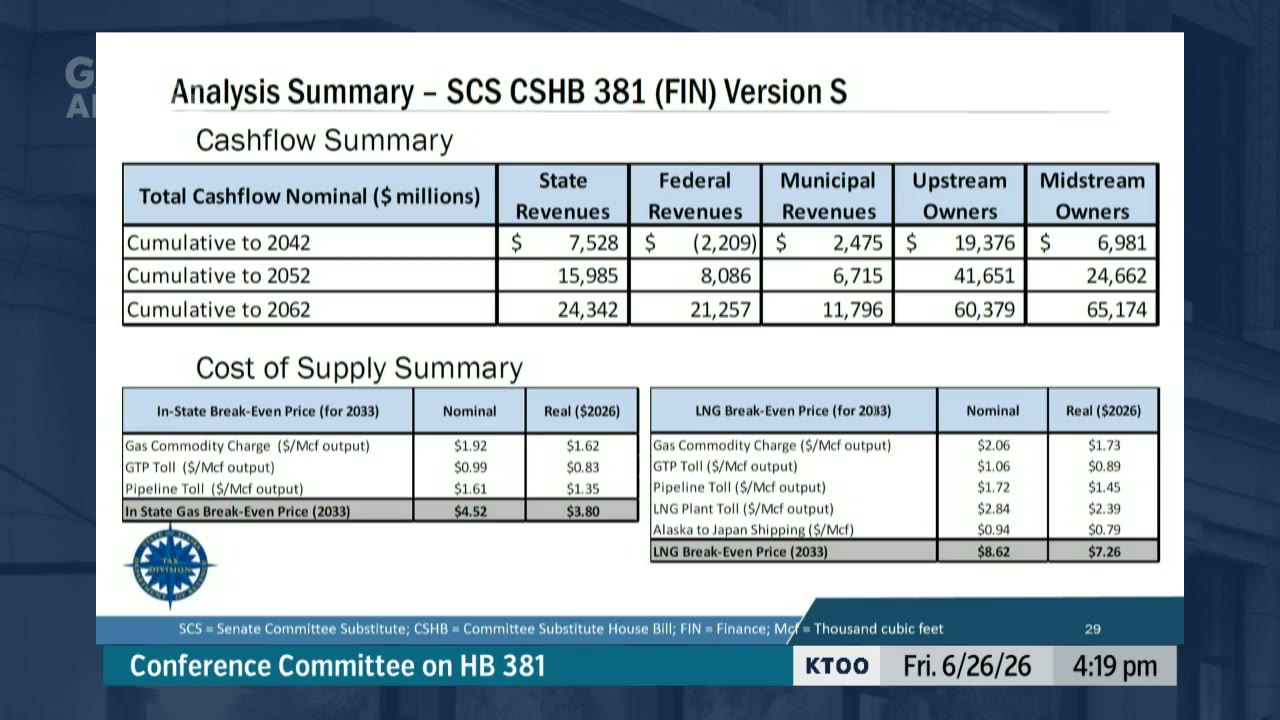

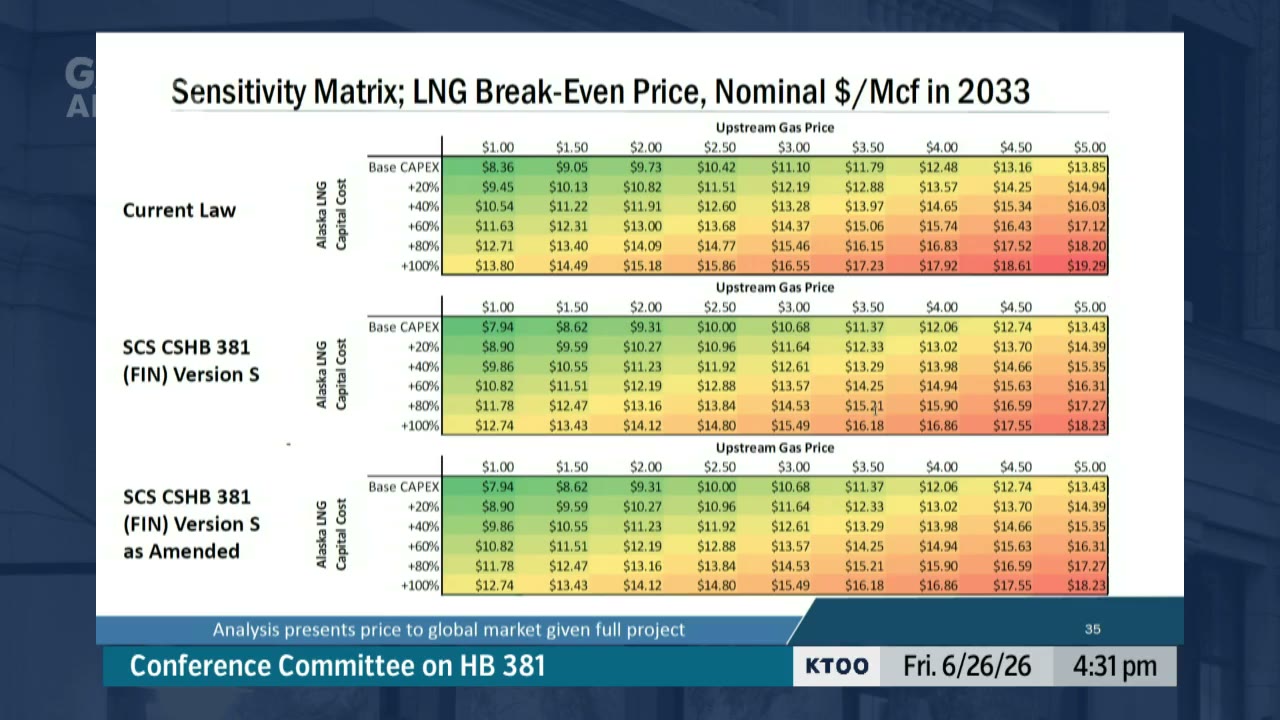

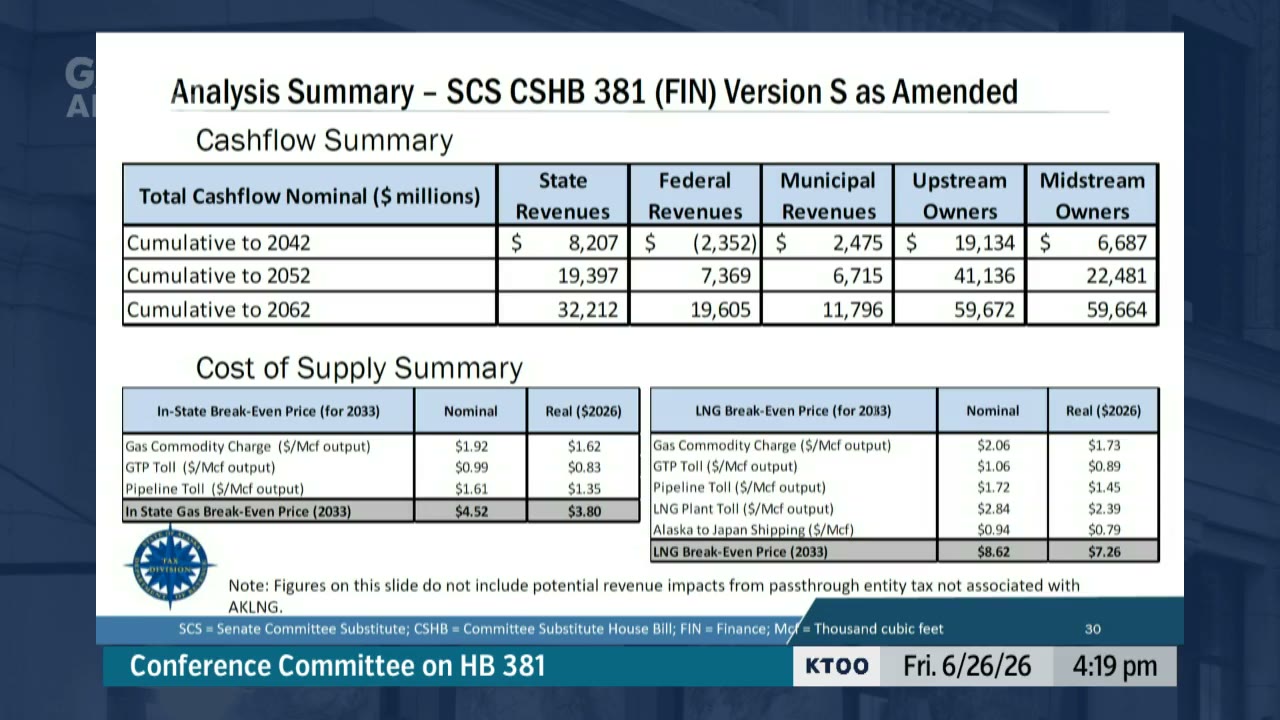

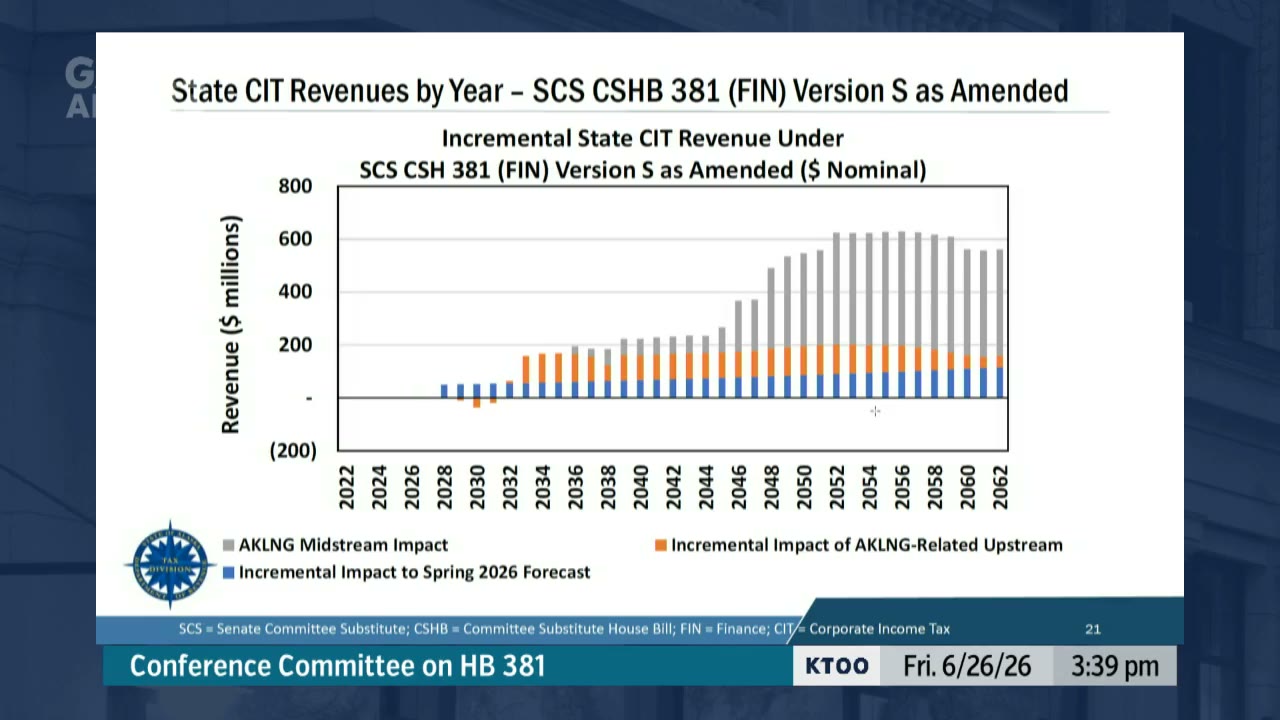

“The— with the alternative volumetric tax that reduces that breakeven price into the global market down to— from $9.05 down to $8.62 per 1,000 cubic feet.”Alaska Legislature: MSC2-20260626-1410

0:42

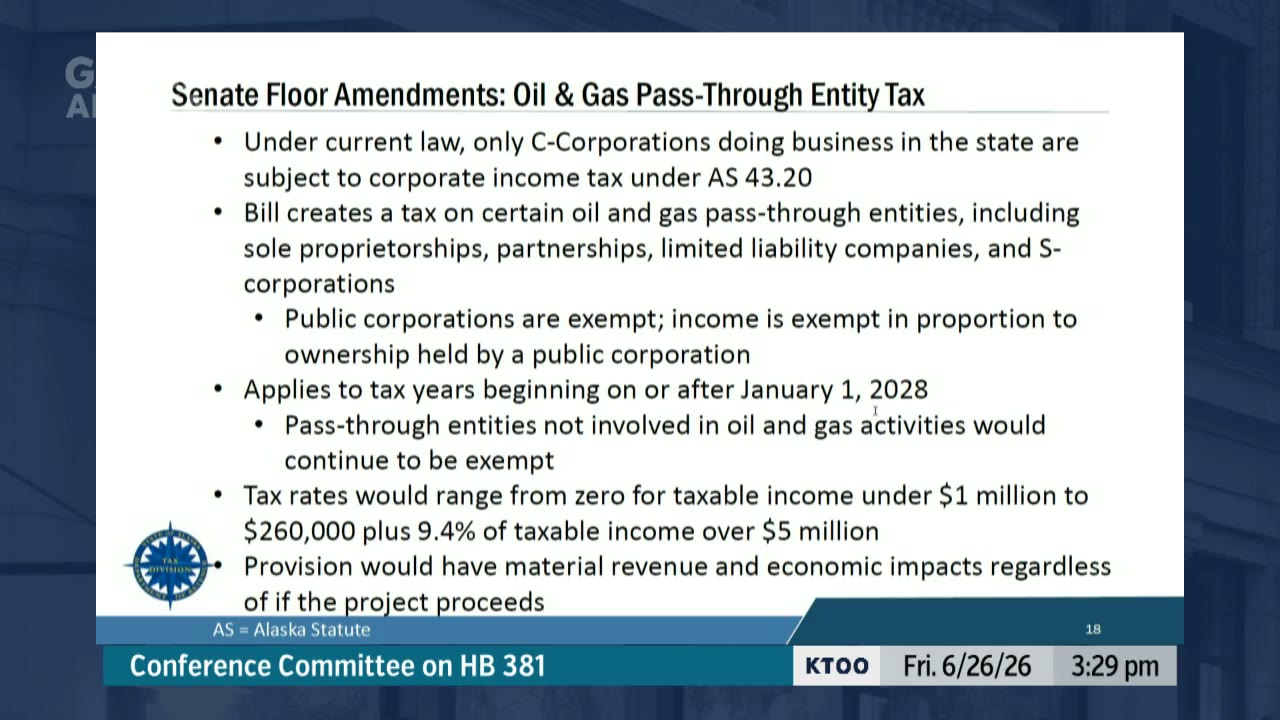

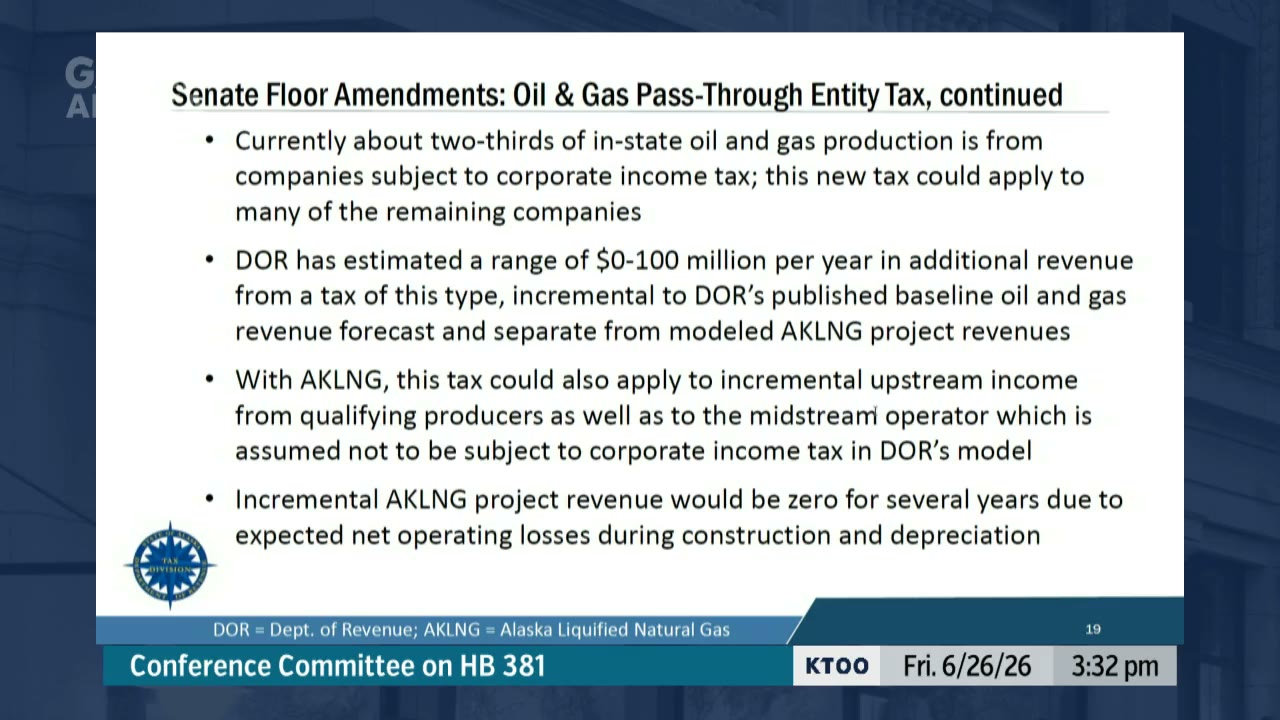

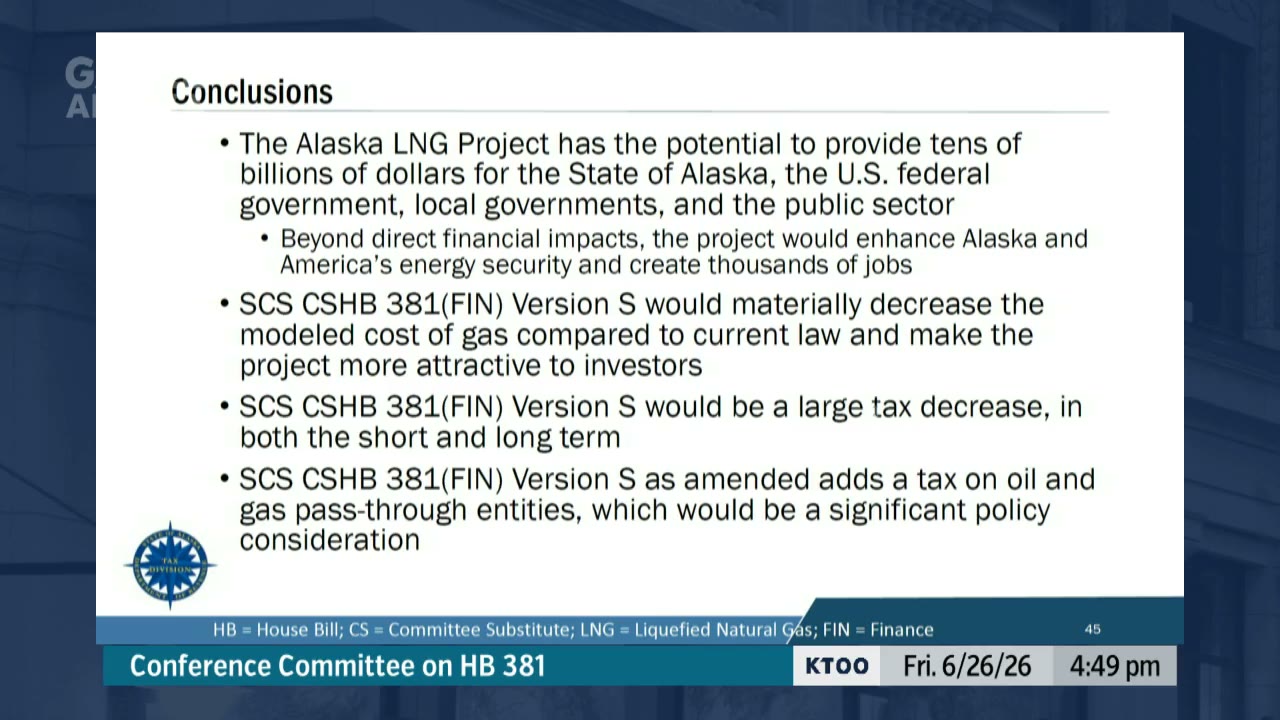

Dan Stickel

“The biggest one of these was the— that directly impacts the Department of Revenue was the implementation of the pass-through entity tax for oil and gas companies. This is a significant policy decision that's before the committee and the legislature.”Alaska Legislature: MSC2-20260626-1410

0:33

Justin Ruffridge

“I think, Mr. Stickel, you're being generous when you say marginal. If the futures market is $8— and we're assuming a $1.50 upstream gas price and we're probably looking at the plus 20% line or the plus 40% line at— in real terms, none of the items I'm looking at on that screen seem to be even in the definition of marginal. It seems like they don't work.”Alaska Legislature: MSC2-20260626-1410

0:36

Bert Stedman

“As far as it being a hypothetical potential of not going forward with the project, I don't believe it's that hypothetical because we've had numerous gas line projects that have not succeeded. This is just the latest one over the last 30 years. And there's a lot of FERC permits issued that never come to fruition.”Alaska Legislature: MSC2-20260626-1410

0:27

Adam Prestidge

“First, in response, Senator Hoffman, you asked about Glenfarm's willingness to continue to pursue the project, and we're absolutely willing to continue to pursue the project, and we will. It doesn't— it creates a little bit of a hesitation around how— around business principles and how, you know, how we will be able to trust certain confidential— confidentiality protections.”Alaska Legislature: MSC2-20260626-1410

0:40

Justin Ruffridge

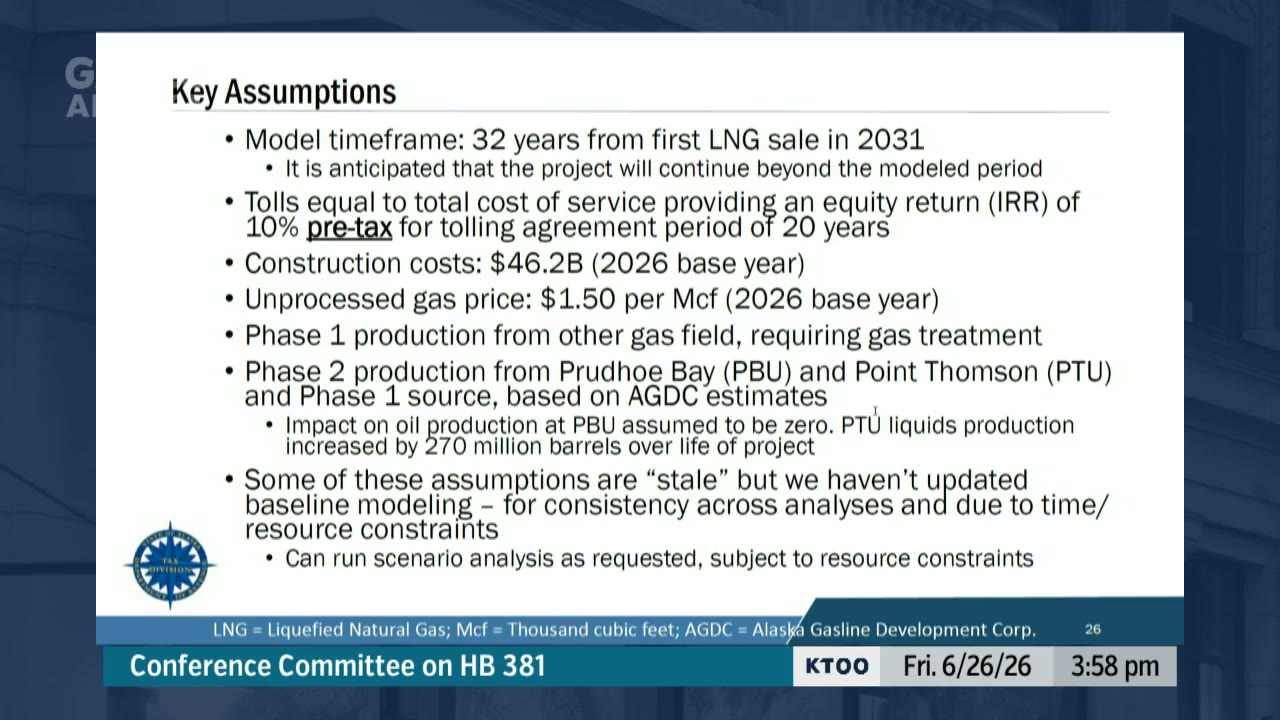

“I really would like to know how much the construction cost, because it seems to me to be a large assumption, weighs into what we're going to see here later, particularly on breakeven prices and other areas of, I think, importance to us as we're making decisions. If the construction cost is higher than what this model has assumed, what main areas does that affect in these following slides?”Alaska Legislature: MSC2-20260626-1410

0:49

Bert Stedman

“when you look at the, at least from what I can gather on the economics of the gas line, with their interest cost and their depreciation, there's gonna be no net income, taxable net income for 2 decades. Literally, 2 decades. So I don't know how that, I guess, will wind up into a tax conversation later on the next couple of days, but you don't pay taxes unless you have a net income.”Alaska Legislature: MSC2-20260626-1410

0:41

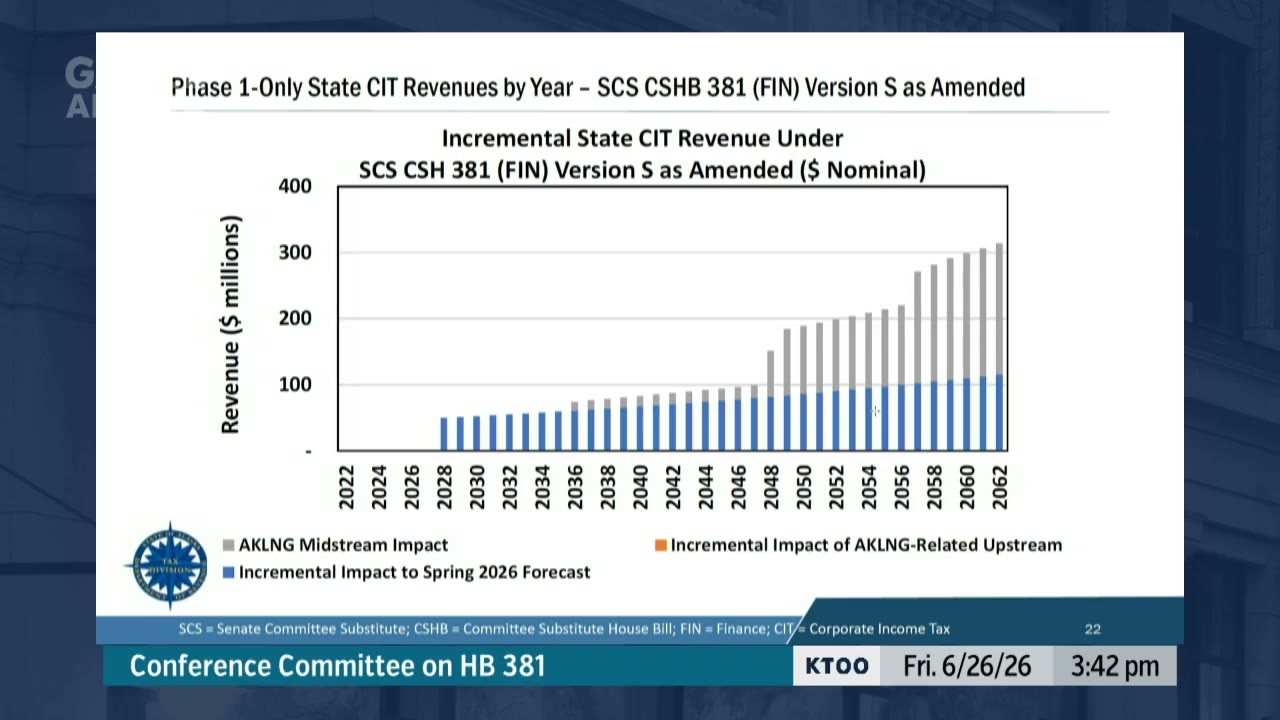

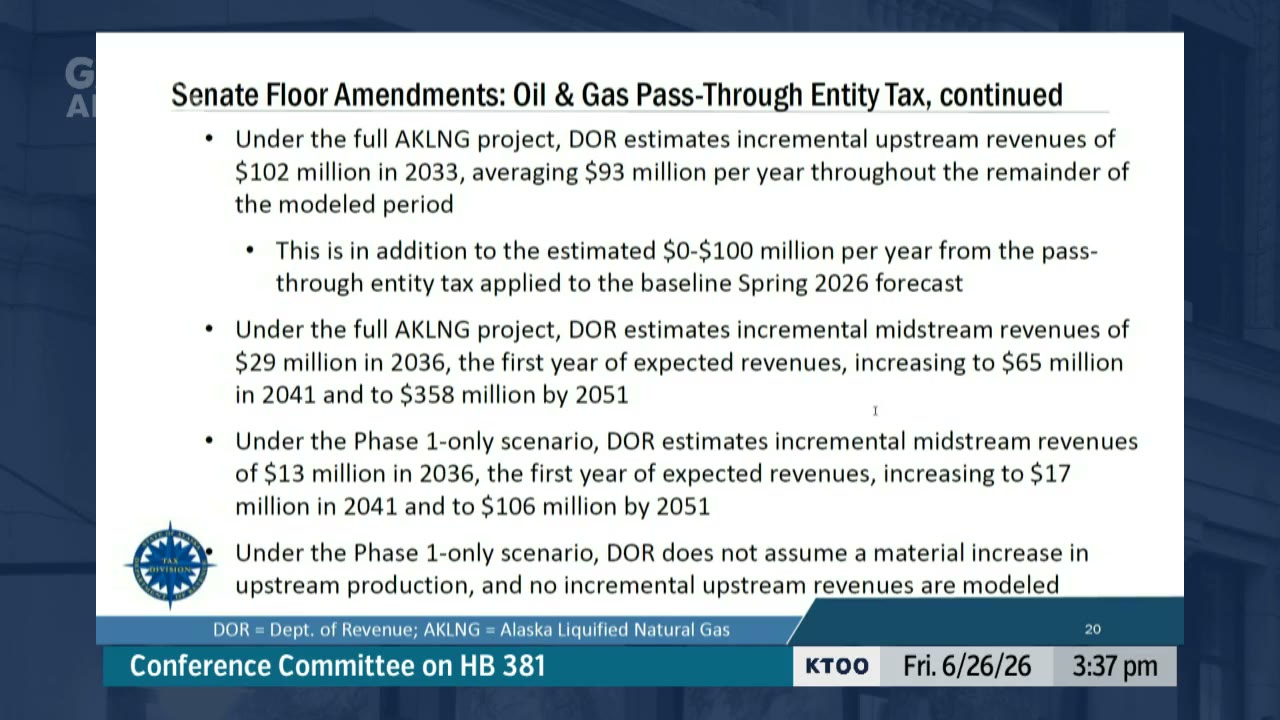

Dan Stickel

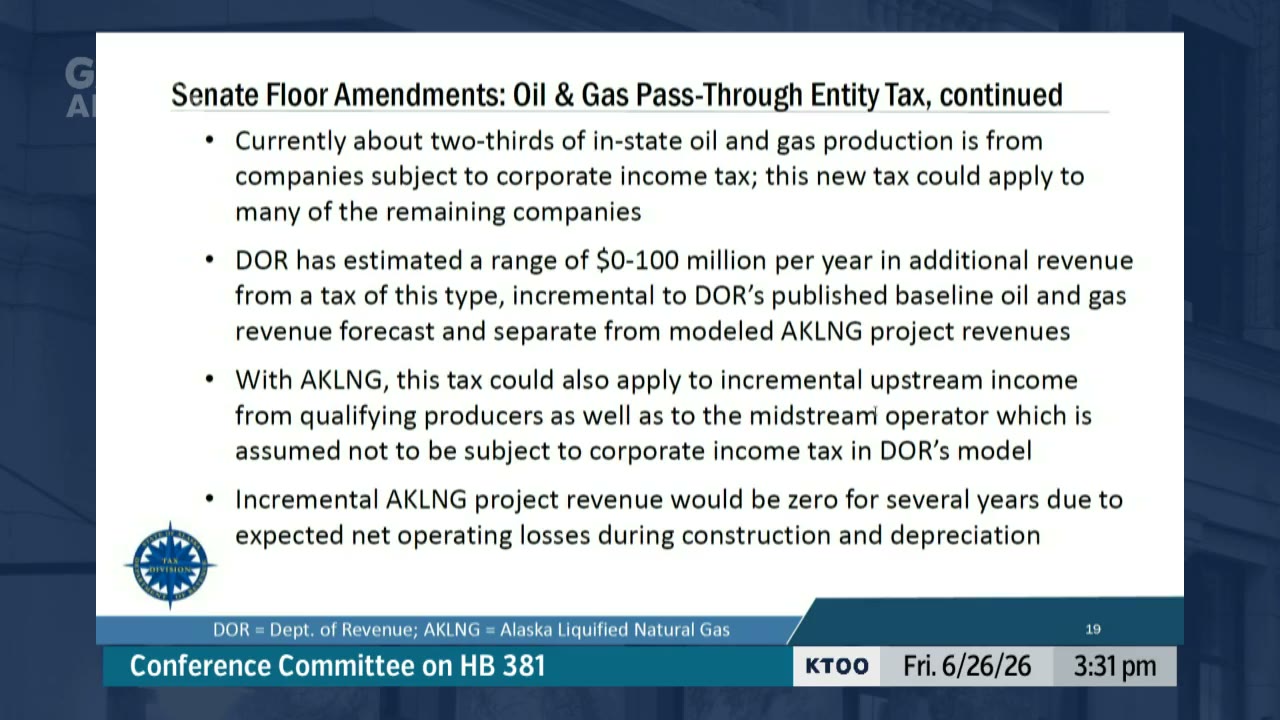

“for that midstream operator, we're estimating $29 million in 2036. That's the first year of expected revenues. That increases to $65 million in 2041 and then up to $358 million in 2051. And what that shift from the 2041 to the 2051 represents is the exhaustion of those carryforward net operating losses.”Alaska Legislature: MSC2-20260626-1410

0:12

Bert Stedman

“they can draw erroneous conclusions from just reading that in isolation. And we've tried to ferret some of that out in our questions.”Alaska Legislature: MSC2-20260626-1410

0:26

Bert Stedman

“I'm sure we'll be looking as we go forward in this process to ensure that there's, um, that it's clearly delineated that there could be no monetary value put on that, um, concession, whatever concessions we make here with property tax. So it won't be left up to an arbitrator in, in arguments.”Alaska Legislature: MSC2-20260626-1410

0:49

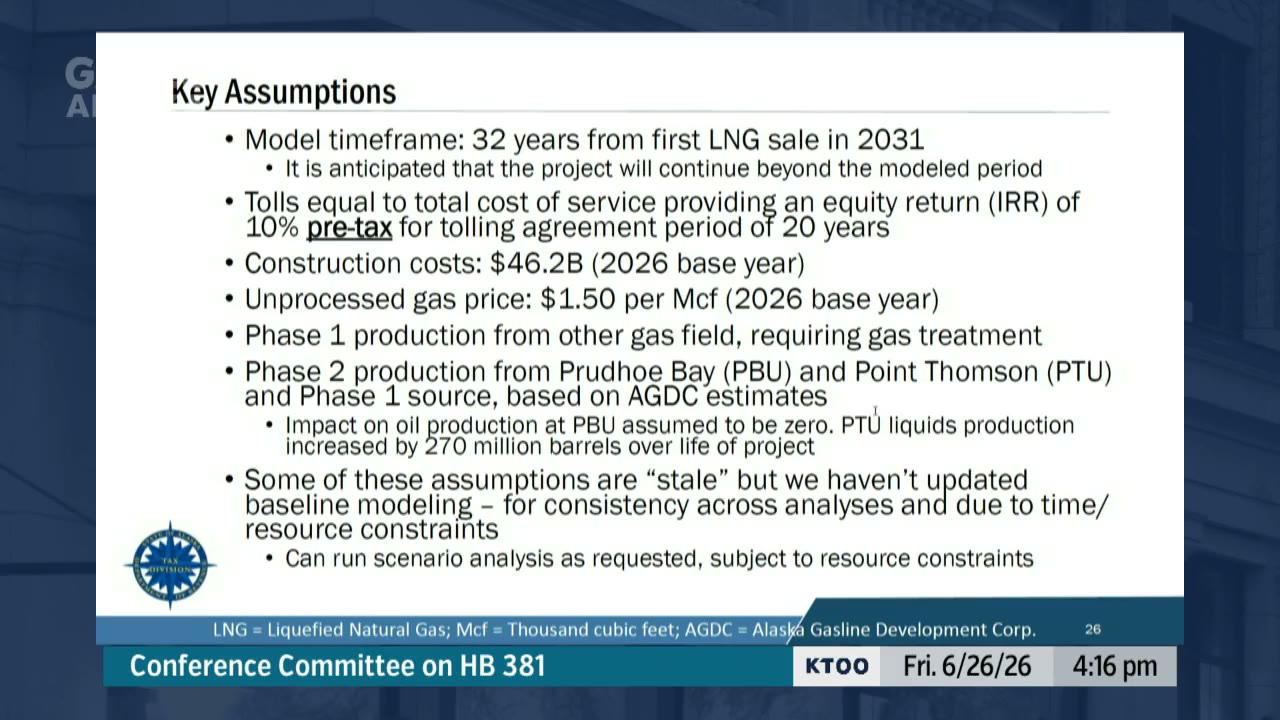

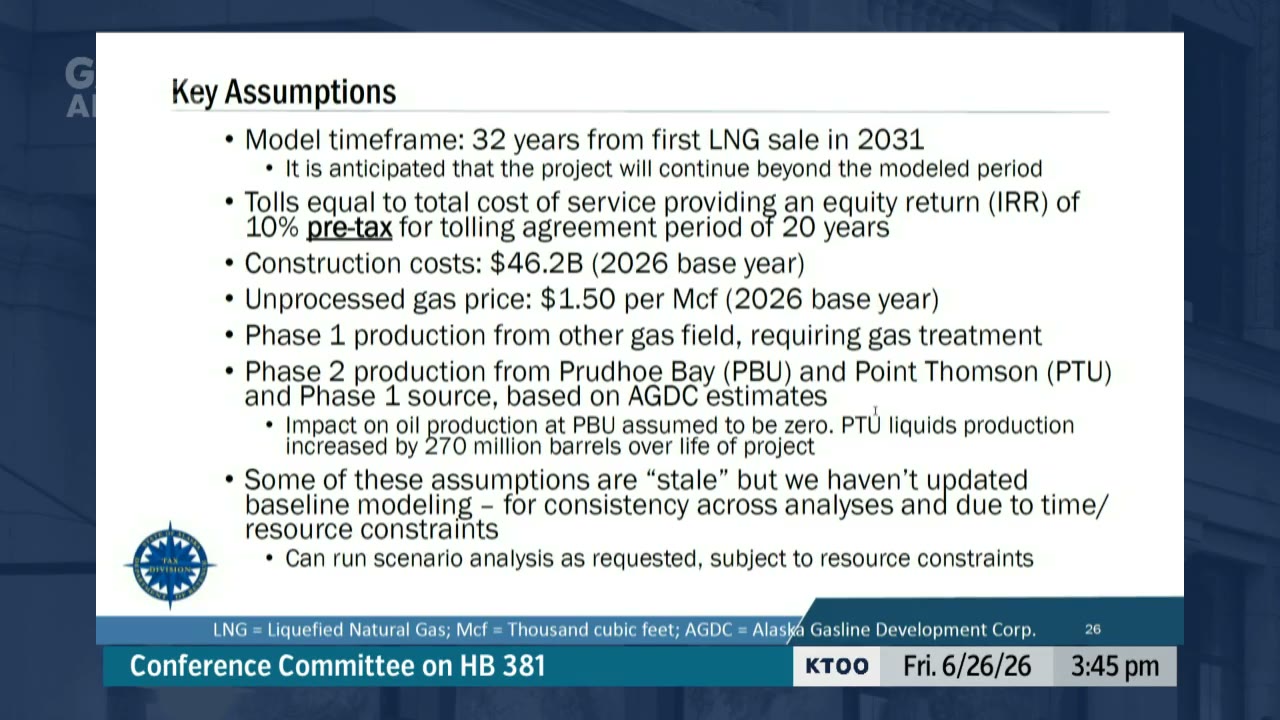

Dan Stickel

“a lot of these assumptions were developed before Glenfarn came onto the scene. We have not received a lot of detailed information and details details on project plan from them, given confidentiality. And so we have carried forward many of these assumptions. There was a significant amount of work that was done in 2018 and 2019.”Alaska Legislature: MSC2-20260626-1410

0:51

Adam Prestidge

“we do have the view that if there were ever a cash consideration or a cash repurchase, we would not ask for the monetary value of any tax arrangement to be reflected in any repurchase. So Glenfarm's position is that you would not claim credit for any value added through tax abatement or other relief from the legislature? Representative Sharkey, essentially yes.”Alaska Legislature: MSC2-20260626-1410

0:53

Dan Stickel

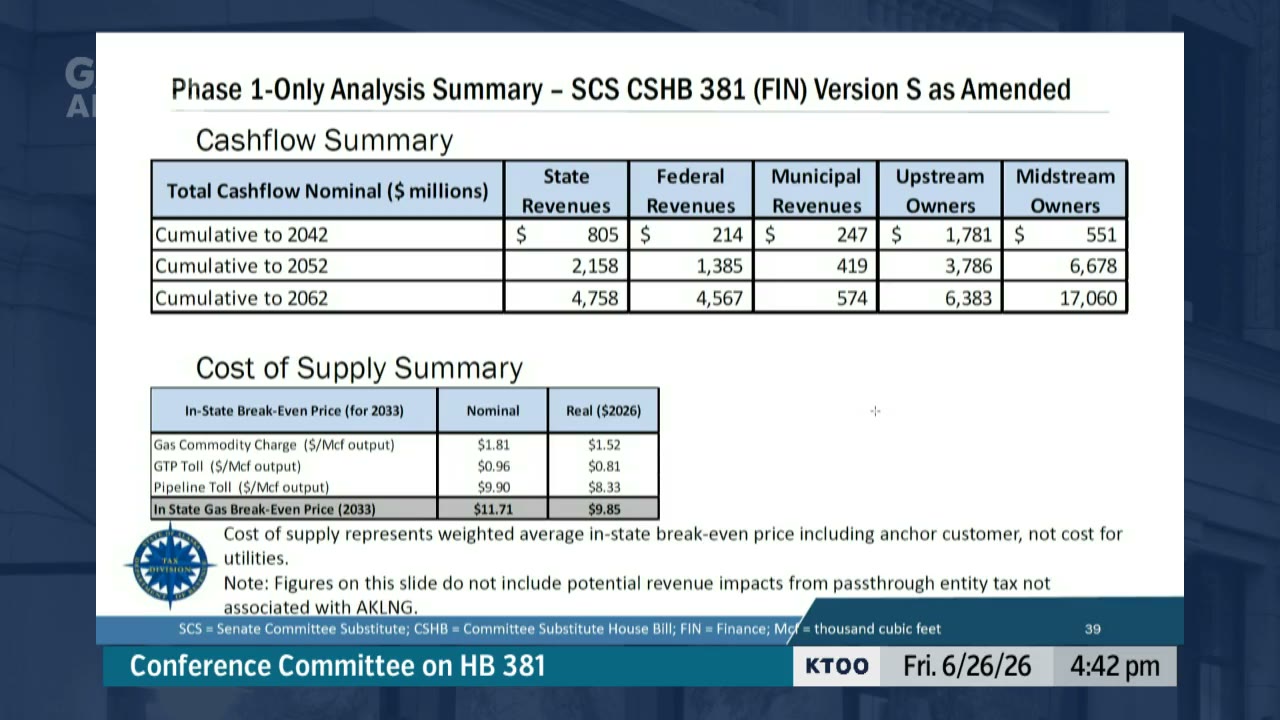

“the upstream and midstream would pay additional corporate income tax with the pass-through entity analysis. A portion of that would be an offset on federal tax because state taxes become a deduction against the federal tax. And then that would shift over life of project a little over— around $6 billion of cumulative revenue would shift from the companies and federal government to the state government.”Alaska Legislature: MSC2-20260626-1410

0:43

Dan Stickel

“The act of agreeing on a new set of baseline assumptions, ideally that would be a months-long process where we would collaborate, we would review all of the latest information in detail, spend some time with it. We would collaborate with stakeholders, partners and agencies, developer, AGDC, industry, and kind of synthesize all of that information. And come up with a new set of baseline assumptions.”Alaska Legislature: MSC2-20260626-1410

0:49

Matt Kissinger

“Representative Fields asked about these clawback mechanisms at that meeting, and what I said was, I said there, I said, and just to address this clearly, This is my words. And just to address this clearly, because I've heard many questions that dance around this, the clawback would be a paid clawback. And there's real important reason for that.”Alaska Legislature: MSC2-20260626-1410

0:42

Dan Stickel

“Representative Ruffridge, through the chair, so that would be a great question to ask the developer, but based on the baseline assumptions that we have and the— what is in the futures market, it does look like a challenging project even with the tax relief.”Alaska Legislature: MSC2-20260626-1410

0:29

Dan Stickel

“broadly speaking, the various, you know, the various versions of the bill have kind of targeted that 50 cents or so reduction to that break-even cost of supply plus or minus 5 or 10 cents.”Alaska Legislature: MSC2-20260626-1410

0:25

Dan Stickel

“in the cash flow summaries, there is a shift of revenue from the federal government and the upstream and midstream into the state government component of about $2.2 billion over life of project.”Alaska Legislature: MSC2-20260626-1410

0:42

Adam Prestidge

“one of our core principles has to do things right by the state, and so to prioritize low-cost domestic gas as low as possible, to do the project as quickly as possible, and more above all, to make sure our contracts and our arrangements with the state are fair to all parties involved. One of those things that we think is fair is the state's clawback option. That's something that AGDC proposed to us in our negotiations.”Alaska Legislature: MSC2-20260626-1410

0:24

Dan Stickel

“We note the significant policy difference between the two versions of the bill is that pass-through entity tax that is in the version that came out of the Senate floor. That does create— that does add a level of uncertainty uncertainty and is a significant policy decision for the committee to consider.”Alaska Legislature: MSC2-20260626-1410