0:46

Alexi Painter

34:35 - 35:22

"it creates Chapter 59 in Title 43. And so the next few slides will use references within Section 18 because that's a very substantive section. So the new Chapter 4359.010 provides a tax abatement, so no taxes at all until the earlier of 500 MCF of daily average throughput for a 30-day period or 5 years after the commencement of commercial operations."

“it creates Chapter 59 in Title 43. And so the next few slides will use references within Section 18 because that's a very substantive section. So the new Chapter 4359.010 provides a tax abatement, so no taxes at all until the earlier of 500 MCF of daily average throughput for a 30-day period or 5 years after the commencement of commercial operations.”

- Speaker

- Alexi Painter

- Timestamp

- 34:35 – 35:22

- Community

- Alaska News

- Location

- Kenai Peninsula

- Captured at

- June 10, 2026

From the transcript

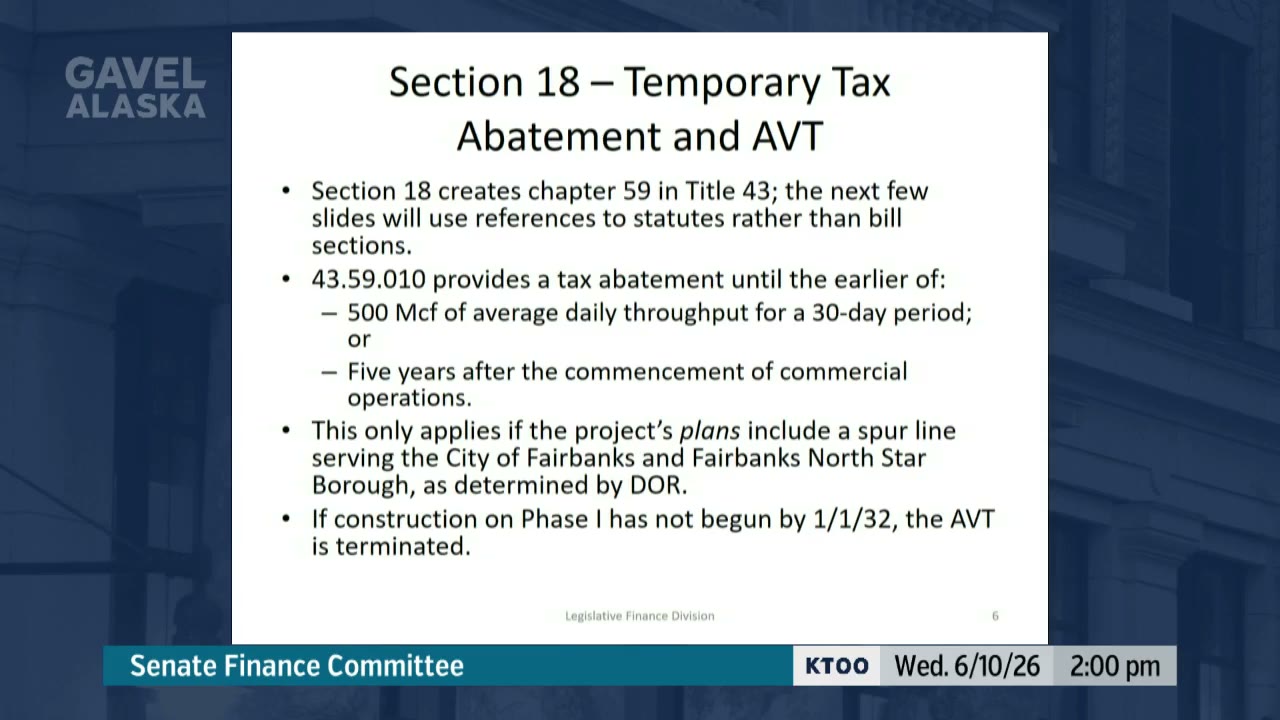

So it creates Chapter 59 in Title 43. And so the next few slides will use references within Section 18 because that's a very substantive section. So the new Chapter 4359.010 provides a tax abatement, so no taxes at all until the earlier of 500 MCF of daily average throughput for a 30-day period or 5 years after the commencement of commercial operations. So there's no tax at all until one of those two things is triggered and then it switches to the AVT. And this only applies— so the abatement itself only applies if the project's plans include a spur line that serves the city of Fairbanks and Fairbanks North Slope Borough as determined by DOR.

Related Coverage

Senate Finance weighs Alaska LNG tax worth $124M a year — and whether it's enough for host communities

Kenai Peninsula Borough Mayor Peter Micciche told the Alaska Senate Finance Committee Wednesday that the House version of the Alaska LNG tax bill provides a workable 70% property tax reduction, while the original 90% cut would have left local taxpayers subsidizing the project.

Juneau, AK, USA