1:05

Alexi Painter

46:21 - 47:26

"revenue begins in FY '31 with just the in-state portion, and then going as the export begins, this higher number."

“revenue begins in FY '31 with just the in-state portion, and then going as the export begins, this higher number.”

- Speaker

- Alexi Painter

- Timestamp

- 46:21 – 47:26

- Community

- Alaska News

- Location

- Kenai Peninsula

- Captured at

- June 10, 2026

From the transcript

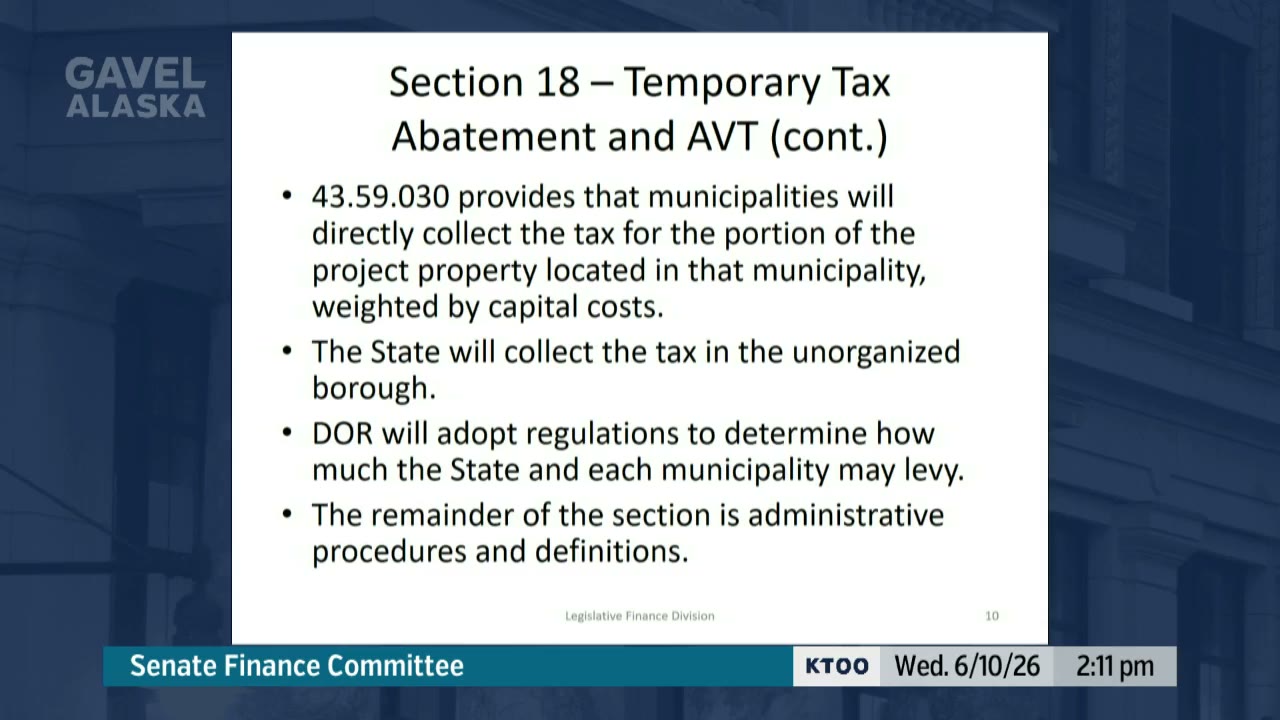

So slide 11, this is data from the Department of Revenue that they were kind enough to turn around very quickly, um, and I appreciate their quick response. So this shows using their base CAPEX scenario and then increasing it by 18% because that gets to the $54.5 billion total to match the Glenfarn High case. And then the table on the top shows the CAPEX expenditures attributable to each municipality, and then to the unorganized borough, that then drive the distribution of revenue, because the taxes collected by each municipality based— weighted on how much of the capital expenditures are in that municipality. The bottom table then shows the revenue summary of where that revenue goes. And so you can see that in the bottom table, revenue begins in FY '31 with just the in-state portion, and then going as the export begins, this higher number.

Related Coverage

Senate Finance weighs Alaska LNG tax worth $124M a year — and whether it's enough for host communities

Kenai Peninsula Borough Mayor Peter Micciche told the Alaska Senate Finance Committee Wednesday that the House version of the Alaska LNG tax bill provides a workable 70% property tax reduction, while the original 90% cut would have left local taxpayers subsidizing the project.

Juneau, AK, USA