Dan Stickel

78:04 - 79:10

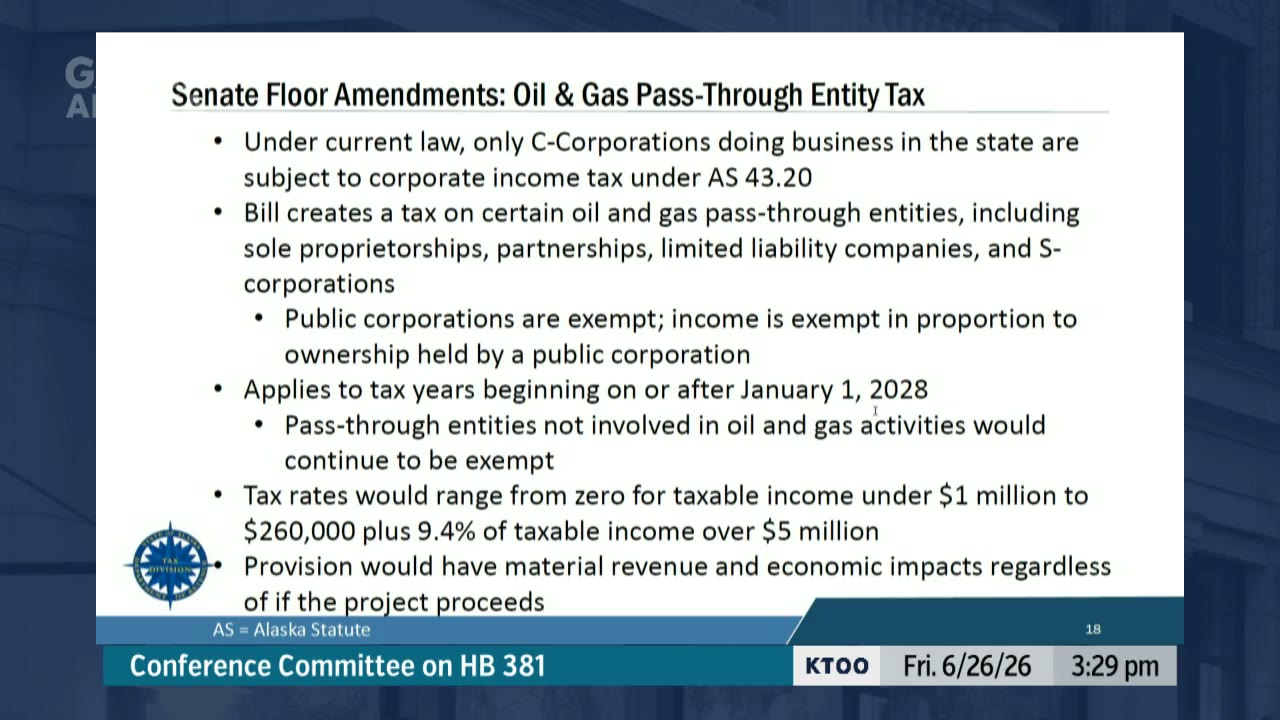

"The pass-through entity tax that came out of the Senate floor applies beginning in 2028 tax year and applies only to oil and gas companies. So a company that's not directly involved in the oil and gas exploration, production, or pipeline transportation would continue to be exempt from state corporate income taxes. There would be a zero tax rate on taxable income up to $1 million per year. Then the top, there would be a series of marginal bracketed tax rates with the top bracket being 9.4% of taxable income over $5 million per year. We note that this would apply to all companies, all pass-through entity companies doing business in the state regardless of whether the AK LNG project moves forward or not and would have material state revenue impacts as well as material investment economic impacts for the impacted taxpayers regardless of what happens with the AK LNG project."

“The pass-through entity tax that came out of the Senate floor applies beginning in 2028 tax year and applies only to oil and gas companies. So a company that's not directly involved in the oil and gas exploration, production, or pipeline transportation would continue to be exempt from state corporate income taxes. There would be a zero tax rate on taxable income up to $1 million per year. Then the top, there would be a series of marginal bracketed tax rates with the top bracket being 9.4% of taxable income over $5 million per year. We note that this would apply to all companies, all pass-through entity companies doing business in the state regardless of whether the AK LNG project moves forward or not and would have material state revenue impacts as well as material investment economic impacts for the impacted taxpayers regardless of what happens with the AK LNG project.”

- Speaker

- Dan Stickel

- Timestamp

- 78:04 – 79:10

- Community

- Alaska News

- Location

- Alaska

From the transcript

The pass-through entity tax that came out of the Senate floor applies beginning in 2028 tax year and applies only to oil and gas companies. So a company that's not directly involved in the oil and gas exploration, production, or pipeline transportation would continue to be exempt from state corporate income taxes. There would be a zero tax rate on taxable income up to $1 million per year. Then the top, there would be a series of marginal bracketed tax rates with the top bracket being 9.4% of taxable income over $5 million per year. We note that this would apply to all companies, all pass-through entity companies doing business in the state regardless of whether the AK LNG project moves forward or not and would have material state revenue impacts as well as material investment economic impacts for the impacted taxpayers regardless of what happens with the AK LNG project.

Related Coverage

Alaska's gas-pipeline bill now carries a tax on Hilcorp and others

The Alaska Senate added a corporate income tax on oil and gas pass-through entities like Hilcorp to the AK LNG gas-pipeline bill (HB 381), effective 2028 regardless of the project.

State economist: even with tax breaks, the gas line barely works

State economist Dan Stickel told a legislative conference committee Friday that the Senate version of HB 381 reduces the Alaska LNG export break-even price from $9.05 to $8.62 per thousand cubic feet — still above current futures market prices near $8 — prompting Rep. Justin Ruffridge to say the project simply "doesn't work."