1:12

Speaker A

28:07 - 29:20

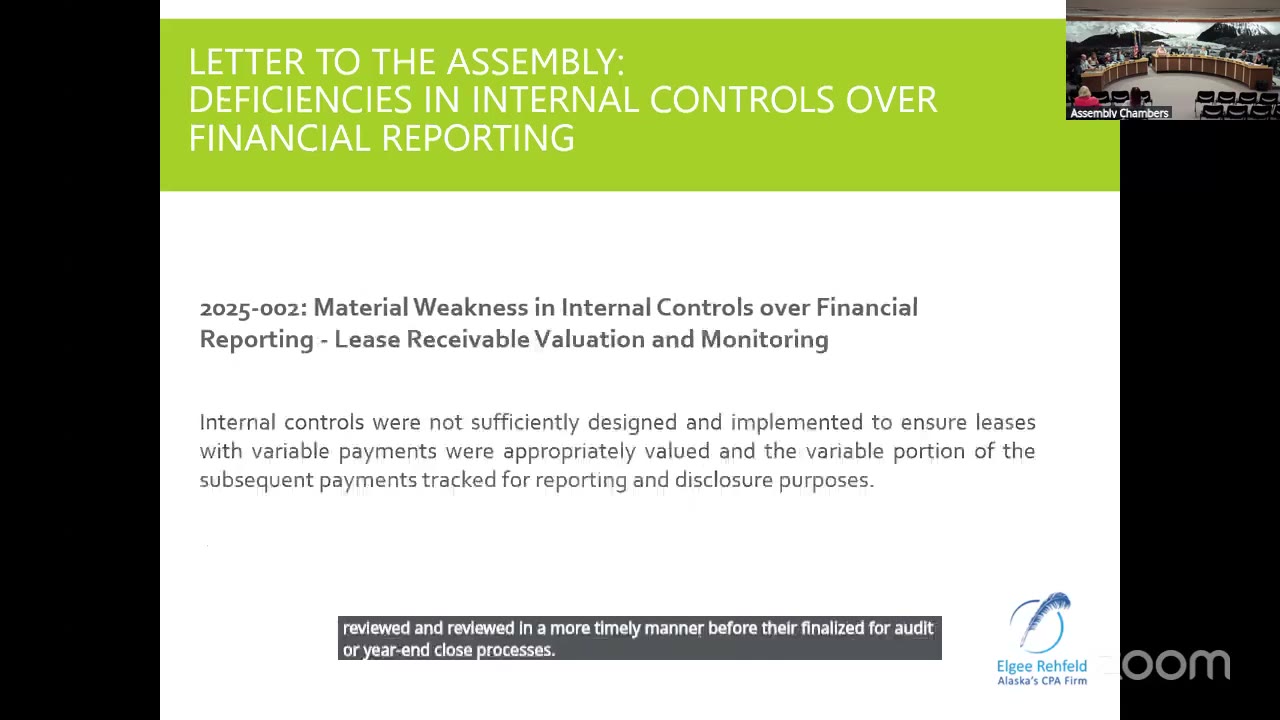

"The second material weakness related to— I mentioned the lease receivable for the Harbors. We found that communication between Harbors and Finance was not sufficient and that there hadn't been adequate review of the variable leases."

“The second material weakness related to— I mentioned the lease receivable for the Harbors. We found that communication between Harbors and Finance was not sufficient and that there hadn't been adequate review of the variable leases.”

- Speaker

- Speaker A

- Timestamp

- 28:07 – 29:20

- Community

- Alaska News

- Location

- Juneau

- Captured at

- June 3, 2026

From the transcript

The second material weakness related to— I mentioned the lease receivable for the Harbors. We found that communication between Harbors and Finance was not sufficient and that there hadn't been adequate review of the variable leases. It's getting really technical, but these are leases that have adjustments every 3 to 5 years, so it may be tied to an appraisal, it may be tied to anchored CPI, right, and that adjusts the value of that lease. And to get into it a little bit detailed is that you include on your balance sheet a lease receivable, and what we found is that when those were initially set up someone estimated what those increases were going to be, and they— so it overstated using GASB's guidance on how to account for variable leases. It overstated the value of those leases because what GASB wants you to do is calculate the value of that lease based on what you know at the beginning of the lease and not take into consideration any of the subsequent adjustments because you don't know what those values are going to be.

Related Coverage

Juneau gets clean audit despite control gaps, three-month delay

Juneau's FY25 audit received an unmodified opinion but arrived three months late due to Bartlett Regional Hospital's audit timing and internal control weaknesses that required millions in corrections.

Juneau